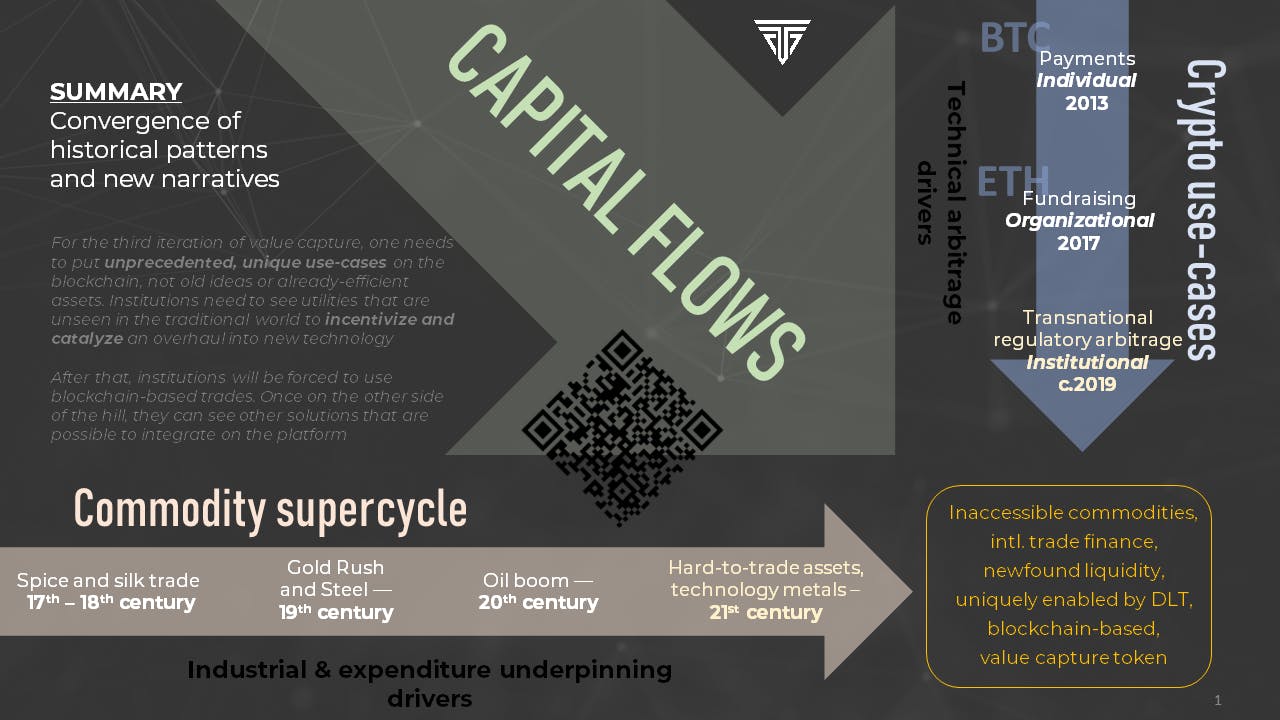

Converging crypto use-cases with capital flows and the commodity supercycle + the quest for the uniquely-enabled app IMPORTANT NOTICE: This document is intended for informational purposes only. The views expressed in this document are not, and should not be construed as, investment advice or recommendations. Recipients of this document should do their own due diligence, taking into account their specific financial circumstances, investment objectives and risk tolerance (which are not considered in this document) before investing. This document is not an offer, nor the solicitation of an offer, to buy or sell any of the assets mentioned herein. Adjectives are important — Killer vs Uniquely Enabled In the search for value in a bear market, the blockchain public is pressed to believe that finding a single sweeping dApp or use case will drive user adoption and, as a result, the value of the underlying protocol. Some have shortsighted hopes to recycle killer but old ideas (Facebook, Uber, etc.) on a newer infrastructure. Blockchain, however, is not about continuing the previous chapter to fit in a Web 2.0 narrative for tech investing convenience. Instead, we look at underlying value drivers to narrow in on where the capital flows have historically and will flow into— on the crypto side to see what has traction ( ) and in the broader economy like Wall Street to see where value has accrued ( , ). The art of hunting for value propositions is to find their catalysts: uniquely enabled use cases, and not “overnight and killer successes.” Jeff Bezos started a before converting that momentum into a modern day infrastructure. thematically technical arbitrage industrial & expenditure drivers Commodity Supercycle very smart online bookstore A carrot on a stick is not enough to convince conservative institutions to adopt: unproven technology negative media coverage regulatory uncertainty expensive infrastructure cost to overhaul current technology systems While protocols can argue day and night about increasing network speed in the far future, this red herring shouldn’t necessarily limit the Enabled use-cases will not only bring unique value onto the blockchain, but will also act as a testing ground for future use cases and familiarity with the DLT platform. invaluable and immediate use-cases that can be provided today. In our report below, we explore one such use case that may possibly supersede the aggregate hesitations given the desperate needs for regulatory arbitrage and access to liquidity in trade finance and commodity trading industries. We dive further into the segments of the industry to find which part is in most need of disruption. process Segmenting trade finance & commodity trading assets Trade finance has been the backbone to globalization and world trade since the dawn of man. Yet the process continues to remains monolithic (to be tokenized), bears onerous reporting (to put on the DLT) and is held back by regulation (trustlessness, disintermediation). Commodities and natural resources underlie all global trade and compose a significant share of emerging markets exports. Copyright AP images — NYMEX open outcry. Trading commodities from orange juice to base metals... many but not all assets can be traded so easily. Already efficient assets such as /base metals, processed oil/gas or USD also fall into a “killer” mentality. Yes, they are the largest and most spectacular, but are they assets in need a solution? How much value is actually enabled by DLT on these popular assets? Fully redeemable, Swiss-vault, extremely accessible to remain competitive. gold gold ETFs (like SPDR) are starting to charge below their own operating costs Instead, and like diamonds, lithium or wood pellets are much more primed for retail access, increased liquidity, price transparency (esp. emerging markets) and tokenization, as many of these assets are not even open for trade to the commodity trading firms themselves. on trade finance is an excellent illustration of blockchain/DLT’s potential in the trade finance and supply chain management space —by unlocking value rather than reducing generic process/cost reduction, back to our point about “uniquely-enabled” diction delineation. For example, if a ship is in process of 3-month long delivery between India to Switzerland, one could trade this dead capital with tokenization to reduce financing & insurance costs. Note that nearly all of the world’s international trade is done . Nevertheless, these process-based, private blockchain solutions have already proven some roadblocks with lackluster adoption rates (e.g. ) that is attributable moreso to rather than a . inaccessible illiquid commodities WEF and Bain & Company’s recent report illiquid overseas, making geographic arbitrage a top priority for commodity traders IBM + Maersk initiative struggles product-design issue target market issue At the end of the report, our team looks into an open-sourced, decentralized solution that not only foils to private blockchain solution as an open access platform, but one that represents a form of liberation from financing banks and their associated legal threads ( Illiquidity, insurance costs, legal protection in trade finance are not results of malicious actors, but from poor mechanized design. So what kind of design would not only improve the system, but allow the public to also reap benefits from this newfound, economic surplus? We dive into a case study through . ie. Basel III, FinfraG, Dodd-Frank, EMIR, REMIT). ABC Platform Case Study Instead of focusing the process-side of trade finance and commodity trading, ABC Platform looks into the tokenization-side of illiquid, inaccessible assets with an thoughtful economic-model through its commodity-based token minting platform. Diving further, Taureon stress-tests the ABC team’s Monte Carlo model against its own bottom-up analysis from management-provided estimates of pipeline partners. The company has already secured a number of brand-name, corporate clients and partnerships which they will announce in the following months. Taureon is excited to see what Mathias and his team will accomplish as they moves toward launching their first product along side industry collaborators (they have to be careful with who they partner with, you wouldn’t want to trade assets with ) blackbox, closed-sourced pricing! In addition to investing and researching the Web 3.0 stack, Taureon continues to explore uniquely-enabled use cases in the blockchain space — from gaming to finance to supply chain to anything. Our team is open to both centralized and decentralized applications with the overlay that they leverage the transformative power of global blockchains as a catalyst of a new economic paradigm. Find the 37-page report here. Note the public report redacted select slides and information per request. (Disclosure: ABC platform is a portfolio company of Taureon Capital.)