275 reads

In-car Payment Systems Unlock New Opportunities for M2M Economy

by Ihor StarepravoJune 4th, 2021

Too Long; Didn't Read

The potential of in-car payments will reach its peak within the machine-to-machine economy of the future. 135 million US consumers spend $212 billion on buying things during their commute. Only 16.7% of actively spending consumers use payment technology built into a connected car. In-car payment technology can provide a more natural purchase experience in sync with the mobility context, with speed and convenience similar to a mobile app. Once Level 4+ autonomy emerges and proliferates the market, in-vehicle payments will leap forward.Companies Mentioned

Coin Mentioned

The line between the FinTech and automotive industries gets blurred even more with the adoption of in-car payment systems. The connected car technology, paired with digital payments, creates plenty of opportunities for automakers and financial service providers. Yet the potential of in-vehicle payments will reach its peak within the machine-to-machine (M2M) economy of the future.

Offering consumers in-car payment systems is a win-win

According to the report, 135 million US consumers spend $212 billion on buying things during their commute. With a convenient in-car payment system at the users’ disposal and a commute-centric application, this number would be higher by 66%.

For now, however, only 16.7% of actively spending consumers use payment technology built into a connected car. Why?

Source: Accenture

We’ve already seen these trends played out with the navigation systems. In the in-car offline vs mobile navigation battle, the first one was seriously hurt.

But after major upgrades from many OEMs, especially in the premium segment, in-car navigation took the lead thanks to its seamless user experience allowing the driver to focus on a single gadget. Now, in-car connected navigation systems boost their driver-use share and unlock new revenue streams for OEMs through data subscription plans.

Similarly to navigation, in-car digital shopping experience with an integrated payment system may soon overtake mobile apps, at least for mobility use cases.

The reason is the in-car payment technology can provide a more natural purchase experience in sync with the mobility context, with speed and convenience similar to a mobile app. Once Level 4+ autonomy emerges and proliferates the market, in-vehicle payments will leap forward.

The connected car commerce partnerships triangle

There are three key technology stakeholders for in-car payment technology: OEMs, financial services providers, and tech companies. Each of them is great in their own domain but can hardly work with each other. Now, it’s time to merge all the three for the sake of connected cars and in-car payments.

The automakers’ task is to tailor the purchase experience to the needs of drivers and passengers. OEMs have to provide their insights into building a driver-centric user experience that greatly improved over the past 5-10 years.

Their expertise in ambient and safe commuting experience for drivers and passengers is much needed for successful payment integration in connected cars. They should also think about a wider car sensory system that may advance user experience. For example, if a user is committing a purchase with a drive-through option, there must be a flow in the car navigation system that takes this event into account altering a route through the pick-up point.

Today, credit card payment and processing companies’ business models are mainly driven by a number of transactions and less so by the total users’ spending.

They do believe that simple “grab-and-go” apps installed in the car won’t make any difference to the number of transactions made through their systems. It means that revenue streams for payment companies can hardly benefit from such applications.

Yet, the accessibility, convenience, speed, and efficiency of an in-car app are a game-changer. Surveys show that 75% of commuters would shop more if the ability to shop and pay was integrated into their car. Following that, in-car payment systems will unlock a totally new opportunity for the M2M economy where the current amount of transactions is just a tip of an iceberg.

The tech companies, in their turn, are responsible for the functional safety of the in-car payment systems. Their understanding of mobility payment use cases is rather limited and needs to be guided by OEMs. To create a smooth driving experience, they both have to take every detail into account, such as the constraints of non-standard on-vehicle electronics, internal communication buses, and scarce on-board connectivity.

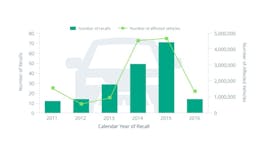

In-car payments: the current state

The major automotive industry players have already formed strategic partnerships to enable connected car commerce.

Honda and Visa’s prototype of a car that pays for goods and services debuted at CES 2017. In 2019, Honda presented a newer version of its connected car with more purchasing and entertainment options. To develop the new in-car payment system, apart from Visa, Honda partnered with PayPal and Mastercard.

Both Visa and Mastercard are actively partnering with tech companies and car manufacturers to create the in-auto payments ecosystem. In 2019, Visa teamed up with a connectivity services provider SiriusXM to build an e-wallet.

Mastercard worked with GM and IBM to create and to integrate car commerce into OnStar systems. In 2018, Mastercard announced its partnership with HERE technologies for combining digital payments and mapping technologies for better connectivity experience.

In January 2020, Hyundai presented its own domestic in-car payment system for GV80. The automaker’s platform uses Genesis Connected Service for wireless connectivity. Currently, the system supports credit cards from 6 companies: Hyundai, Shinhan, Samsung, Hana, BC, and Lotte. For now, you can use a GV80 car as a wallet to pay for gas and parking only.

Security and privacy of in-vehicle payments

Safety is paramount in the user experience design in all mobility applications. So, to win the consumer’s hearts, in-car payments systems have to be functional but safe in all possible ways.

The National Highway Traffic Safety Administration’s data shows that 33,000 Americans were injured in 2018 in crashes involving cell phones use or other cell-phone related activities.

While mobile app developers can’t do anything about these statistics, automotive players have a real chance to significantly offset the number. Thanks to the advancing voice-activated controls, the in-car payment system enables less driver distraction. With the forthcoming Level 4+ of autonomy, self-driving cars will become even safer for commuters who want to spend their time in a car for shopping.

From a security standpoint, a typical in-car payment system is somewhat similar to mobile systems. It’s vulnerable to the common wireless mobile payment system and protocols threats, such as malware, data breaches, transmission channel security vulnerabilities, etc. And it withstands using similar techniques and approaches such as multi-factor authentication, data safeguards, fraud detection, and prevention.

There are, however, a few peculiarities for the in-car payment system.

First, a car is a quite noticeable object with legal connections to its owner. Therefore, fraud attacks will require a bit more than just stilling your card number. The car can become your viable alternative authentication unit.

More and more cars are featured with driver monitoring systems (DMS) that will enable new security related features through driver recognition. Super multi-factor authentication can be very intuitive for the user and add extra security planes to the in-car payment system.

Privacy consideration is the major threat to an in-car payment system. Modern cars keep tracking a lot of personal data (including current user location and future routes).

This data is essential for marketing and e-commerce use cases (purchase along the track, local promo, etc.) and also becomes a major target to malicious users. OEMs protect such data by embracing onboard secure storage and HW-enforced encryption. Such applications require Over-The-Air updates as a core functionality to ensure continuous onboard application security.

M2M economy of the future

Current development of in-vehicle payments enables many new use cases that are lucrative enough for OEMs, tech companies, and credit card providers. Yet, the true power of the in-auto payments ecosystem and a strong kick to the economy will take place with the proliferation of M2M payments. The car, or better say, the onboard artificial intelligence, will become an active economic actor.

Perhaps now, the idea of using cars as buyers and merchants on the owner’s behalf sounds a bit strange and disturbing. How can one let robots be in charge of financial merits? Well, in some industries, such as high-frequency trading, machines have a long and successful track record of making millions of transactions and generating billions in profits. Researches show that AI takes care of finances even better and smarter than humans.

Source: Gartner

The future of in-car payments is connected with a cooperative mobility concept where vehicles will not only initiate parking or fuel transactions but also pay and get paid for the valuable real-time data such as traffic, weather or even sensor data and its interpretation.

In the cooperative driving environment, machines will buy such data from other machines using currencies that could, for example, be implemented as geofenced blockchain. Autonomous cars will form a distributed, flat-hierarchy, and super-scalable compute engine that will create an ecosystem for the future Industry 5.0.

To sum up

Now, we witness the early days of in-vehicle payments technology. It’s not yet accessible, and it has miles ahead before mass-market adoption. But the future of in-car purchases is bright and promising. With the autonomous car technology, payment systems will leap forward.

Interconnected autonomous cars will become economic agents and make purchases from other machines for humans. With the help of smart vehicles, we’ll create a safer, faster, and more convenient driving experience. I am truly excited about the future of in-car payments, are you?

L O A D I N G

. . . comments & more!

. . . comments & more!

About Author

TOPICS

THIS ARTICLE WAS FEATURED IN...

RELATED STORIES

24 Stories To Learn About Automotive #automotive

Jul 29, 2023