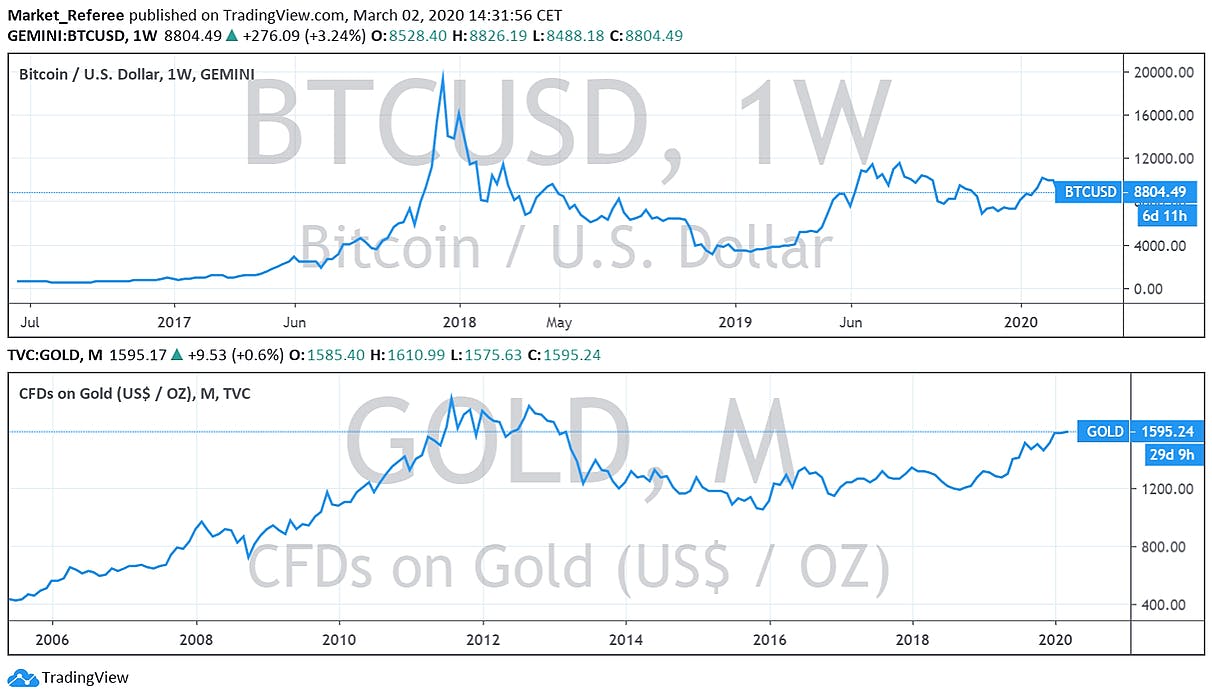

The last month will go down in history as "black February" and not so much because of volatility in the markets as growing geopolitical tensions. Despite all the promises, Russian President Vladimir Putin gave the green light to a so-called "military operation" in Ukraine. It didn’t take long for Europe and the US to respond. In a matter of days, the Office of Foreign Assets Control of the US Department of the prohibited United States persons from engaging in transactions with the Central Bank of the Russian Federation, the National Wealth Fund of the Russian Federation, and the Ministry of Finance of the Russian Federation. Treasury This action effectively immobilizes any assets of the Central Bank of the Russian Federation held in the United States or by U.S. persons, wherever located. On top of that, the United States and its allies have announced that they are prepared to restrict imports of Russian technology products by 50%. Lose-lose situation The only problem is that anti-Russian sanctions have also punished the global economy: gas and oil prices are skyrocketing, whereas prices for metals, including palladium, which is widely used in the manufacture of automotive catalysts, have hit multi-year highs. In this context, it shouldn’t be a surprise that inflation expectations have spiked once again. According to the latest , Eurozone consumer prices rose by a record 5.8 percent in February. data The jump in the cost of living in the Eurozone to well above the ECB’s 2 percent inflation target has divided the central bank into two groups: those who are pushing for tighter monetary policy to tackle inflation and those who want a pause to assess the economic impact of Russia’s invasion of Ukraine. Prepare for High Gas Prices Regarding energy prices, the biggest issue is that the world's leading oil powers simply cannot increase production due to lack of capacity because of extremely low investment in the industry in recent years. Even the current quotas are not fully taken by OPEC+ countries. The good news is that the prospects for the Iran nuclear deal remain important for the oil market. Negotiators are gradually moving closer to a consensus, which could mean the removal of sanctions on Iranian oil exports and would add up to 1 million barrels to the market by 2022. Iran currently produces about 2.5 million b/d. It is forecasted that the rapid growth of commodity prices could end up pushing up inflation in the U.S. and EU. The monetary authorities will inevitably react to this by raising refinancing rates, which will raise the cost of loans for businesses. Given the rise in the cost of industrial raw materials, along with energy, this will inevitably lead to a downturn in the global economy. In particular, JPMorgan Chase & Co. a run-up to $150 a barrel would almost stall the global expansion and send inflation spiraling to over 7%, more than three times the rate targeted by most monetary policymakers. warns How to Save Money Despite rising inflation expectations, the major cryptocurrency failed to justify its safe-haven status. Possible reasons for the continuation of the sideways trend include geopolitical tensions, as well as increased hawkish sentiment at the Federal Reserve. If risk-off in the markets continues, Bitcoin's return to historical records may be delayed. In the meantime, Exchange-traded funds that in gold and other precious metals have seen massive inflows. Data from Refinitiv Lipper showed and other precious metal ETFs have seen an inflow of $4.7 billion this year, after witnessing outflows worth $7.8 billion last year. invest gold Regarding the stocks, the best idea would be to follow Buffett’s principle: not to rush and invest in enterprises with a long-term economic outlook. It is worth mentioning that in the last quarter, Berkshire Hathaway shares of Teva Pharmaceuticals (TEVA) and Sirius XM Holdings (SIRI), and bought securities of Formula One Group (FWONK), Activision Blizzard (ATVI), and Nu Holdings (NU). sold In addition, Berkshire increased its stake in Chevron (CVX) by more than 33%, decreasing its stake in Kroger (KR) by 0.61%, and Charter Communications, Inc. (CHTR) by 8.8%. Also, the company continued to get rid of pharma securities, with shares in AbbVie ( ) down -79%, Bristol Myers Squibb (BMY) down -76%, and Royalty Pharma (RPRX) down 34%. ABBV Another option would be to invest in real physical assets: real estate, cars, or bars of gold or other metals. In addition, it could be a good idea to focus on businesses that don't depend too much on market conditions and external circumstances. Everything that generates cash is a possible defense against inflation.