4,213 reads

Why Doesn’t Anyone in Crypto Think About Distribution?

Too Long; Didn't Read

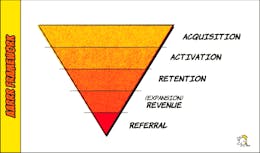

Cryptocurrencies are global and accessible. No sign-up is needed, and you can start interacting with a permissionless <a href="https://hackernoon.com/tagged/blockchain" target="_blank">blockchain</a> to move cryptocurrencies from user account to user account without a middleman — or counterparty. However, most cryptocurrencies rely on network-effects business models where the <a href="https://hackernoon.com/tagged/cryptocurrency" target="_blank">cryptocurrency</a> is only as good as those who use and accept it.Companies Mentioned

Asheesh Birla

@ashgoblue

L O A D I N G

. . . comments & more!

. . . comments & more!