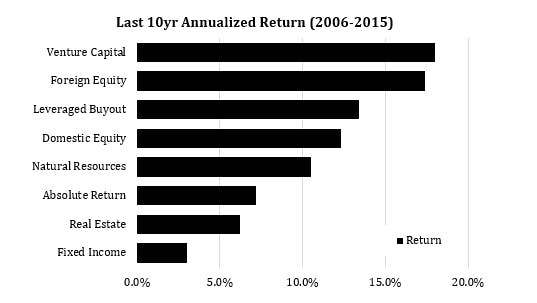

As a former entrepreneur — I often thought about the “how” and “why” of venture capitalists. I also wondered if their job was really that hard or if they were just riding the money train. Now that I’ve gone to the “dark side” and become a myself — I (hopefully) understand this much better. VC Understanding the of being a VC will help explain some of the questions entrepreneurs may have including: math Is the job that hard? Don’t they just golf, cycle, or kite surf all day? Why do they care so much about ownership percentages and check sizes? Are they just scheming to throw me out? Why are they so obsessed with unicorns? Shouldn’t they care if my company turns $10M into $100M, that’s 10x! I’m a scientist/engineer by training so I always like to look at things analytically. The limited partners (LPs) of venture funds typically have the following minimum expectations of their venture asset class investments at the completion of a fund (typically 10 years): Seed/early stage — 3–4x returns (12–15% annualized) Early/mid stage — 3x returns (10–12% annualized) Late stage — 2x returns (6–8% annualized) As a general comparison, LPs can obtain 1.5x returns after 10 years on many different types of asset classes including private equity, public equities, and real estate. LPs look to venture capital to provide premium returns due to the increased risk and illiquidity of the asset class. For riskier and longer term investments like seed funds, LPs expect an even higher premium. Otherwise, there is no financial reason to give money to venture firms. Historically, many venture funds do fail to hit these targets, and a large proportion also fail to return 1.5x or even 1.0x. Let’s see how this plays out with a hypothetical seed/early stage firm called Dough Ventures. They just raised a 3rd fund, Dough Ventures III LP, with $100M in total cash. For LPs at the end of a standard 10 year fund, Dough Ventures needs to return $300–400M in cash. That doesn’t sound horrible does it? Let’s look at how returns are generated. There is a concept in venture called the — where most of the funds’ returns are generated by very few (sometimes one) investments. It’s all about investing in the “home run winners.” There are very few big winners. Power Law Dough Ventures typically targets a 10% ownership stake in the companies it invests. On average, they write checks of $1.0–1.5M for companies with pre-money valuations of $8–12M. Let’s assume across the portfolio, Dough Ventures owns 10% equity stakes for all companies. Fast forward 5–10 years: the portfolio matures and the successful companies exit at IPO or via M&A. What does the total enterprise exit value of the portfolio need to be to hit the target return metric of $300–400M? ; 10% of that value is $300–400M. The answer is $3-4B Returning the Power Law, statistically, 10% of the portfolio will be drivers of fund return. For a typical portfolio of 20–30 companies per fund, 2–3 companies will drive all the gains. For Dough Ventures’ portfolio, those 2–3 companies need to be worth $1–2B each, returning $100–200M to the fund per investment. Data compiled by Correlation Ventures showing the historical distribution of returns. 10% of financings provide over 5x return while 65% are partial or complete write-offs. This is why you hear investors asking questions relating to market size/TAM, and potential revenue, comparables, etc. They are trying to understand if your company has the potential to be a company that will be valued at $1B or higher, i.e. a unicorn. A fund needs a few big winners to hit the return metrics that the LPs demand of the VCs. The strategy and math change for a $10M or $1B fund, but the concepts are still the same. future It is important that the VC invest in companies that have the potential to “return the fund” because they need every investment to have the possibility to be a big winner. It’s nothing personal, it’s just math. Relatedly, you may also hear some VCs say a $100M exit is a “failure.” While this wording is harsh and partially disconnected from reality, an exit of this value will not do much to move the needle on providing fund returns. If Dough Ventures had a company exit for $100M, with 10% ownership at exit, they obtain $10M in returns. However, if the goal is to return $300–400M, $10M is only 2–3% towards that goal. Let’s examine another scenario where Dough Ventures invests in 20 companies: 10 exit for $100M, 10 exit for $50M. This would seem like a rousing success since all 20 companies exited for decent amounts. However, in doing the math, assuming 10% ownership, Dough Ventures only nets $150M in total, providing for a sub-par 1.5x fund return. On the flip side, let’s say of those 20 companies, 19 go bankrupt but 1 company exits at $5B. Assuming 10% ownership, the fund returns $500M for a 5x fund return. placing it in the upper decile. This is why the Power Law in venture is important. In reading this, you can probably infer some of the key metrics which can have an effect venture return math: — larger funds can have a harder time providing high multiple returns because of the exit valuations needed (a $1B fund needs $2–3B in returns with exit values of $10–30B) Fund size — early stage companies have lower valuations that can enable higher ownership percentages Stage — lower ownership percentages proportionally increase the exit valuations needed to hit return metrics (a 2% ownership at exit nets you 5x lower returns than 10% ownership) Ownership percentage — small checks result in low ownership percentages Check sizes — A fund’s ownership percentage will decrease in each round and be diluted unless investments occur Follow-on funding/dilution pro rata — VCs want to see potential revenues higher than $100–300M annually and TAMs at least in the $10Bs in order to have confidence the company can reach a $1B+ valuation at exit Market size/TAM/revenue Boiling that all down, this is why VCs ask the questions they do — it all comes down to determining these parameters for the math equation. In reality, the numbers are not always in the VC’s favor: : Grabbing 2–3 unicorns in a portfolio is no small feat as many funds do not even have one at the end of a fund cycle. For Dough Ventures, a 10% hit rate would be considered a success. There are other funds who take a “spray-and-pray” approach to portfolio construction, but typically those funds cannot place high enough ownership percentages to take advantage of the winner. Picking winners : For Dough Ventures, $3-4B in total value at exit may not seem too bad considering ~$50B is returned in VC annually on average. However, most of this money is locked up in a few big winners. Think about how many companies have exited for $1B+ each year in the last 10 years. Exit enterprise value : Many funds can start out at 10–20% ownership in a company, but if a it raises large sums of capital to scale the business, that requires deep pockets to maintain that ownership. With the exception of the flagship funds like NEA or Sequoia, that can be a hard task due to fund size constraints. Ownership : VCs charge fees like any other investor for operations. Those fees reduce the cash returned. The actual return net of fees must be even higher than the target metric to compensate. So a 3x return may actually need to be a 4x return on invested capital. Net vs gross returns It is also important for founders to understand what VC investors are thinking as they evaluate an opportunity. That is just how the math pans out. This is why it’s so important for VCs to pick entrepreneurs, technologies/products, and markets that have the potential to scale up to be a $1B+ company. Of course there are many companies that will be smashing successes, but just won’t provide “venture returns”. Founders should not take it personally. I’ve turned down some companies I knew would be great outcomes for the founders, but it just didn’t make the math work for our fund. Finding other investors who are not beholden to LPs (say angels or family offices or even corporate investors) are a great way to build those businesses up. This was a very simplified run down of how the math works and there are plenty of nuances, adjustments, and variables that come into play. Perhaps another article another day on that.