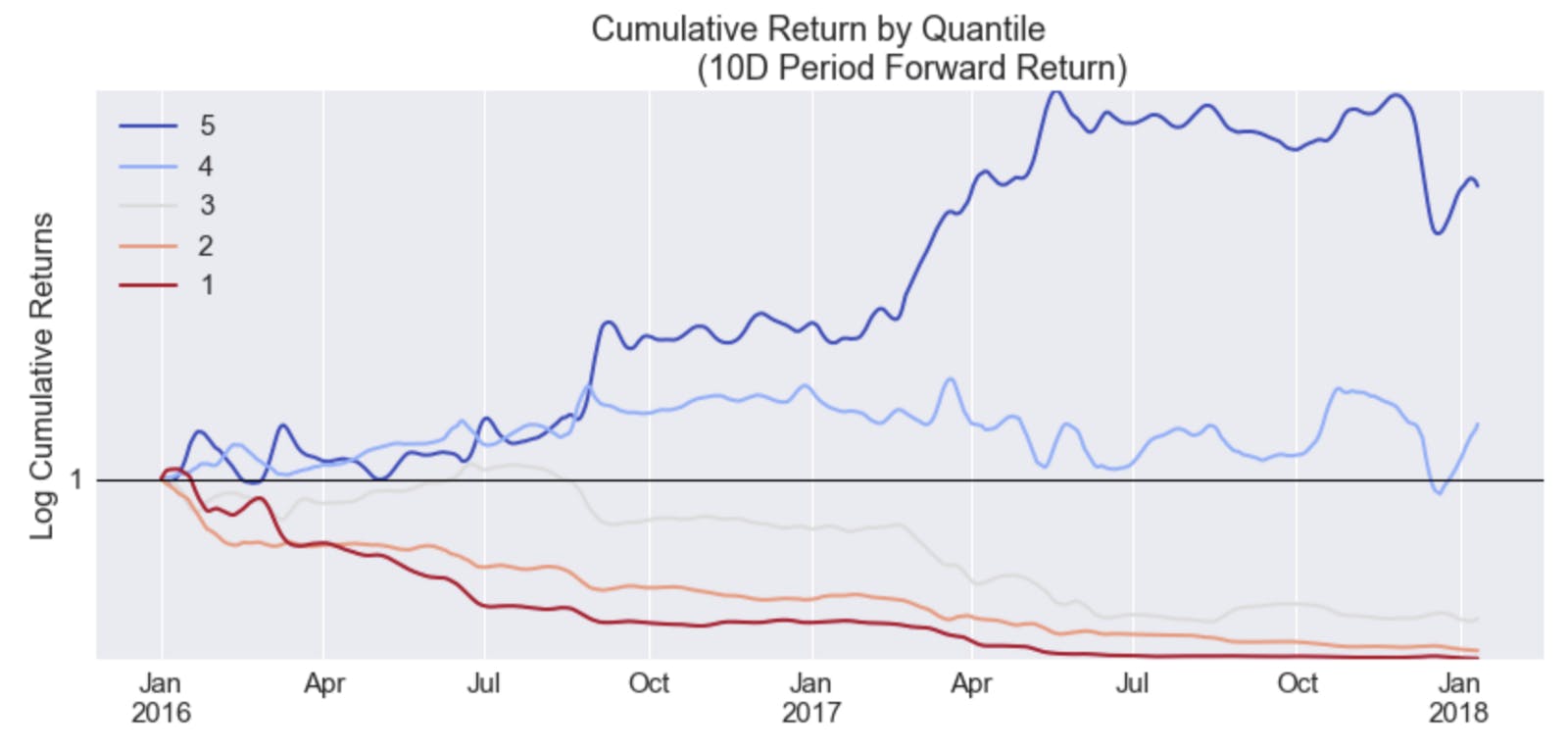

A Statistical Analysis of Relative Momentum Strategies This is the second in a series of posts on using quantitative models to help inform investment decisions in the crypto asset class. Click here to see the first. Momentum trading is a trading strategy in which you buy assets that have gone up in price and sell assets that have decreased in price. The idea is that price trends are likely to continue, and thus, a strategy of simply buying assets in an uptrend and shorting assets in a downtrend is consistently profitable. There are three main behavioural and structural reasons that underpin the anomaly: Information is both diffused and acted on slowly by market participants Liquidity forces large investors to spread out transactions over time Humans extrapolate recent performance leading to herd mentality My illustrated how a relatively a simple version of momentum has been quite predictive of short-term returns for a basket of ten crypto assets over the last 5 years. Specifically, we looked at time-series momentum (TMOM), which simply looks at the price of an asset in isolation. Essentially, if the price of the asset had increased, an asset is said to have positive TMOM, whereas if it had decreased it had negative TMOM. previous article Relative Momentum This article will go a step further and look at relative momentum models. Relative momentum models compare the performance of an asset versus its peers to determine momentum rather than simply looking at the asset in isolation. This is slightly more complex, and thus hopefully more predictive. We’re going to stay consistent with the previous article, and use the same universe of ten crypto assets: , Litecoin, Ethereum, Ripple, Dash, NEM, Dogecoin, Monero, Vertcoin, and Bitshares. We’ll also use the same window for calculating momentum (past 10-day performance) and calculate it on a daily rolling basis. Bitcoin Relative momentum is different than time-series momentum in that it requires ranking the assets in the universe into different baskets. We then compare the average future 10-day returns of each basket over time. The logic is that the top basket (i.e. the assets with the highest momentum) will consistently outperform the bottom basket (the assets with the poorest momentum). We split the universe into five baskets (also called quantiles). The top basket (quantile #5) represents the average future 10-day returns of the top 2 assets, while the bottom basket (quantile #1) represents the weakest two. The results for running this test for 2017 are below: As we can see, the results are pretty much exactly in line with the hypothesis. The quantile with the highest momentum outperformed by 639 basis points (i.e. 6.39%) more than the average, while the lowest quantile underperformed by 4.53%. This means buying the two assets with the highest prior 10-day price performance and shorting the bottom two assets would have netted an average 10-day return of 10.39% in 2017 for our universe (assuming no costs though!). That is an extremely large return spread that you would never see in traditional equity markets. Repeating this test in 2016 for our universe brings similar results: Again, the top momentum quantile outperforms by 3.12% while the weakest momentum quantile underperforms by 3.47%, resulting in a 10-day long-short spread of 6.59%. Interestingly, in both years, average returns increase monotonically across quantiles as momentum increases. This is a sign of a significantly predictive factor. Putting all of this together into an actual long-short strategy would have resulted in a portfolio equity line looking like this: A factor-weighted long-short portfolio (i.e. long strong momentum and short weak momentum) would have resulted in a 2-year return of 540%. While the volatility would have been quite high by normal standards with a 50% drawdown in late 2017, relative to simply being long crypto, the volatility is actually less. This makes sense given that this momentum spread exists because of long-standing behavioural/structural reasons while crypto assets are based on a large amount of speculation. Investors that want exposure to both crypto and the momentum anomaly can simply go ignore the short-side of the equation and go long high-momentum crypto assets. Conclusion Similar to the previous article on time-series momentum, the consistency in the results is surprising, with pretty much a one-to-one relationship between relative momentum and average future returns. The message is once again clear: expect crypto assets that outperform to continue outperforming, and for weak performing assets to continue being weak. We believe the crypto markets to be incredibly inefficient, meaning that simple strategies like this are actually highly profitable avenues for market participants to trade. Long-term investors can utilize these types of models to better time entry and exit points, and improve their risk management. Further areas that I’ll explore in this quantitative crypto series: combining time-series and relative momentum into one (i.e. ), the more advanced , on-chain transaction , alternative valuation models using measures of community size, combining sentiment with momentum, and much more. These are all datasets we’re already collecting for our own internal use and models we use to help inform our personal investment decisions. dual momentum residual momentum valuation models