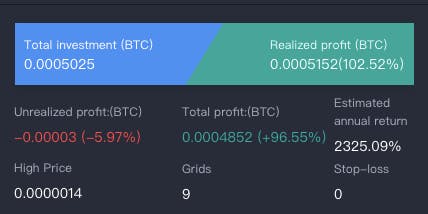

Prices move in a wave like fashion, moving back and forth following a broader trend. While doing so, it often revolves around a mean. It might move across or bounce off the mean. Mean reversion systems are designed to exploit this tendency. Prices much above the mean are considered expensive and the ones below the mean are considered cheap and the positions are taken accordingly. This back and forth movement of prices or the standard deviation needs to be high enough to make profits otherwise the system might fail. There would not be much room to take profits if the volatility is very low. Costs such as slippage, brokerage etc. will make it difficult to remain profitable. We will first look at frequency distribution of prices of Bitcoin and visualize the mean reversal tendency through curves. Then we will move on to create a simple counter-trend strategy for the prevailing trend in the crypto space. Statistical Evidence for Mean Reversion : Rather than using frequency distribution of prices itself, we have calculated frequency distribution of hourly returns. Lets look at some of the statistics that I obtained after analyzing hourly price returns for BTC/USDC pair trading on Coinbase from 13th November 2018 to 5th April 2019 and BTC/USD pair trading on Coinbase from July 2017 to April 2019. It can been seen that the graphs are not perfectly Bell Shaped. It is worth noting that the values are very tightly distributed and it resembles a double exponential distribution.With a little tolerance mean, median and mode are almost equal. Quoting mathworld.wolfarm.com : “Reversion to the mean, also called regression to the mean, is the statistical phenomenon stating that the greater the deviation of a random variate from its mean , the greater the probability that the next measured variate will deviate less far. In other words, an extreme event is likely to be followed by a less extreme event.” It can be seen in the Fig. 1.1 & Fig. 1.2 that, the further we move away from the mean returns, the value of probability distribution function decreases, making the probability of having further higher deviation in returns less probable. This might not be the best example to explain mean reversion but here we can see the tendency of periodic returns to return towards the mean which can explain the validity of mean reversion of freely traded instruments. How does mean reversion compare with trend following strategies? An attempt at building my own Mean Reversion Strategy for Crypto Currencies: Disclaimer : This resource is for educational purpose only and does not constitute a recommendation to buy, sell or otherwise deal in investments or trading. Entry Condition : SELL when RSI MA(14,close,triple,2,0) crosses below RSI MA(14,close,simple,10,0) and 14 RSI higher than 70. Exit Condition : BUY at stop loss of 1.0% or target profit of 2.5%. Cryptos have been in a bullish trend recently. Here we are trying to create a bearish strategy to demonstrate how corrections in prices can be traded within a broader general trend that is against our direction of trade by trying to catch the mean reverting moves. RSI higher than 70 condition is used to check for overbought levels. Since RSI itself is a very volatile indicator, we smoothen its value by applying averages. Then we check for crossover of the smoothened RSI values when the RSI is already in the overbought region. Crossover of a smaller period MA with a larger period MA is checked for fading short term relative strength. And when the setup is complete, we go short. Instead of defining mean and taking profits at the mean, to keep the strategy simple, profit taking is done on fixed %. The strategy was backtested to evaluate the performance. While it does not work for all the pairs, it performs well on some other pairs. Here are some of the successful backtest results : It can be seen in the above images that against a positive period return of 16.26%, the short strategy has managed to make 7% returns by doing 4 trades out of which 3 were profitable. The backtest period is 03/17/2019 to 04/16/2019 and it is carried out on 10 min candle interval. Conclusion While there are evidences mentioned in the article suggest that mean reversion works in freely traded markets, there is a lot of room for further research. Simple strategies can be created to trade counter to the direction of trend and also for the periods of sideways trends. Traders must consider to diversify their strategies across trend following and mean reversion which might be helpful in reducing drawdowns or risks associated with using just one kind of strategy. Bibliography : for backtesting strategies and charting. https://streak.world for defining mean reversion. http://mathworld.wolfram.com/ReversiontotheMean.html The data used to calculate the probability distribution of price changes can be downloaded by clicking on the tickers , . BTCUSD BTCUSDC

![featured image - Mean Reversion Trading Systems and Cryptocurrency Trading [A Deep Dive]](https://hackernoon.imgix.net/images/un1ei2b7q.jpg?auto=format&fit=max&w=3840)