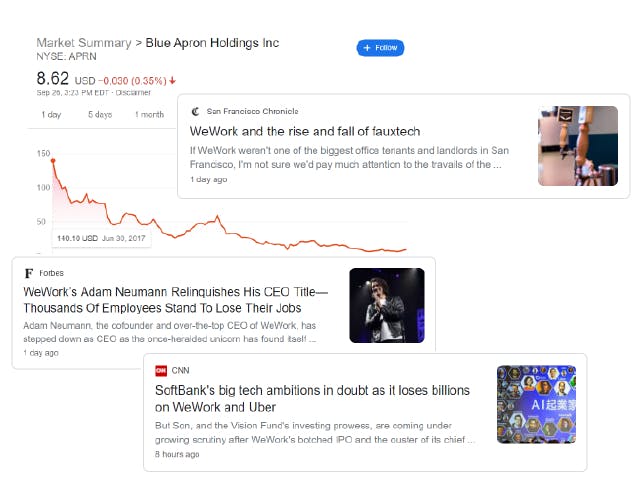

Startup founders' dreams are often filled with massive fundraising rounds, IPOs, and high valuations, and their nightmares with crashing stock prices and angry VCs. WeWork and Blue Apron have long been the type of company many founders look up to, but they seem to be facing their demise in 2019. How do companies with so much initial promise crash and burn so quickly? And how do we avoid the same fate? Customer Retention Many companies (and investors) focus on sales and customer acquisition so much that they forget one of the golden rules of business - it's than it is to gain a new one. While meal kit services were the "next big thing" for a while, Blue Apron and friends were losing as many as within the first 6 months. 5 times cheaper to keep an existing customer 72% of their customers That said, SaaS companies today should focus on both sales retention to avoid falling into the trap of endless and unprofitable acquisition. Constantly check in with your customer support teams and improve your product's onboarding and customer education. The former will lead you to the problems you can solve to improve retention, the latter will ensure customer success - a key to preventing churn. and Profitability There's a lot to say about the lack of profitability in many modern startups. A relatively recent trend fueled by investors drawn to higher risk (and higher return) investments has led to companies like Uber and Lyft posting massive losses year-over-year and somehow still continuing operations and fundraising. The antithesis of free-market capitalism, these companies are able to lure in customers with unsustainable pricing with the help of massive capital, pushing companies with sustainable business models but fewer financial means into the dirt. In WeWork's case, the company managed to turn a traditionally profitable business model (commercial renting) into losses with . With investors throwing a massive amount of money into the business, WeWork could afford to take losses. That is, until it all came crashing down. Now investors are looking for ways to drive long-term returns on WeWork without ex-CEO Adam Neumann. expenses over $1 billion in just 6 months Blue Apron's stock prices caught an upswing just after by changing up both their operations and accounting strategies - laying off part of their workforce and using non-GAAP accounting practices. A boost in Blue Apron's stock price after indicating they'd finally meet a basic tenet of good business is a major sign that reaching profitability isn't a trend in the startup and investments world. Their abysmal lifetime stock performance proves that the market won't sustain bad business models forever. claiming they'd be profitable in Q1 2019 The moral of the story in this case is remembering that outside funding can't save your company from an unsustainable business model. Investors can seem like an endless source of future capital that give companies a false sense of security and guaranteed growth. A focus on profitability from the very beginning, with or without investors, will ensure your company can hang on in the long term. Of course, if you're just looking to execute on a 5-year exit plan, you just have to make sure you exit before shit really hits the fan. Over-Valuations & Unnecessary Hype A huge seed round is a big sign of success for startup founders. Many people have a "the bigger the better" mindset i fundraising, but valuations and investor attitudes change over time. Blue Apron commanded a valuation of about $2 billion while it was raising capital in 2015. Now, (as of September 26, 2019), its total stock valuation is closer to $60 million. WeWork's IPO dreams were crushed after years of multi-billion dollar valuations. trading at around $9 per share How does such a massive discrepancy happen in valuations? One clear explanation is the difference in venture capitalists' and traders' attitudes surrounding a company's performance (or expected performance). A valuation in a company's early stages is much more indicative of investors' optimism, while stock valuations represent real-time expectations and performance judgement. Another explanation is that startups tend to generate a lot of hype in the early stages, and it's much harder to maintain once the business model is seen in action. Before crunch time, business models, revenue predictions, and TAMs rule valuations. Innovative ideas command a lot of hype, but that doesn't directly translate into actual revenue or success (see Theranos). Once a company gets going, expectations meet reality and hype is replaced with concrete evidence. Avoiding this particular struggle is complex because it requires that founders keep a realistic view of their company and future expectations regardless of how investors and industry experts are treating them. Getting attention from Forbes or landing a spot on the NYSE would make anyone feel like their company is a massive success. A new star-struck founder may be over the moon about a VC's valuation or willingness to invest, forgetting that investors can't predict the future either. A strong strategic plan with contingencies based on fundraising can help keep your feet on the ground. SaaS startups are uniquely scalable, but trends of non-profitability and pre-revenue hype in the startup space can lead companies into an Icarus-style trap. Crawl before you walk, walk before you run, and run before you fly to avoid flying too close to the sun and burning.