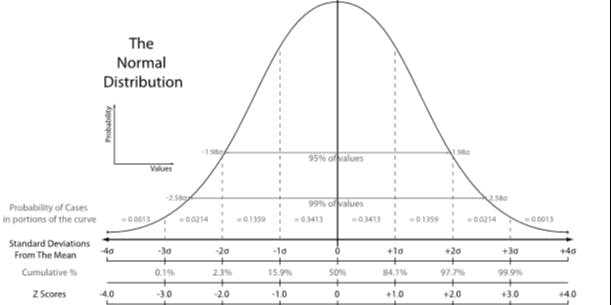

Financial markets are chaotic. So chaotic, even, that many economists and investors believe market trends to be the product of ‘random walks’ and that prices cannot be predicted ( ). But randomness shouldn't be worrisome. In fact, random price movements can be good. Gaussian random walk, an assumption used by an options pricing model called Black-Scholes, treats intervals of an asset’s price over time as independent variables. By doing so, the changes in price over time, or the returns of an asset, are assumed to be normally distributed. Otherwise stated, “If transactions are fairly uniformly spread across time, and if the number of transactions per day, week, or month is very large, then the Central Limit Theorem leads us to expect that these price changes will have normal or Gaussian distributions” ( , 399). When an asset's returns are normally distributed, the probabilities of those returns are known. Knowing these probabilities can give investors a reliable framework accounting for the risk of holding said asset. When it comes to bitcoin, . The purpose of this article is to explore how to frame risk and to test how well traditional assumptions, implicit in derivatives pricing, apply to bitcoin. see generally Malkiel Fama much has been said about how risky it is This article will proceed by introducing the derivatives market and giving an overview of the Black-Scholes model. After a brief discussion of why the Black-Scholes model is important and what it does, I will highlight the weaknesses of the model and the (sometimes) unrealistic assumptions it makes. I will then turn to how well the model fits into the bitcoin derivatives market. Particularly, I will show that historical data on daily bitcoin returns from January 2016 till August 2019 exhibit Following a discussion of the findings, I will compare the efficacy of Black-Scholes applied to bitcoin with the S&P 500. Finally, the article will end with closing thoughts on why the Black-Scholes model may poorly fit the crypto market and the implications this presents for the future of the quickly growing crypto derivatives market. excess kurtosis . Derivatives and Hedging Away Risk Imagine that you’re a farmer and you expect to produce 5,000 bushels of corn. Naturally, you want to sell the corn for as much as you can. However, because prices are subject to the demands of an unrelenting market, there’s a possibility that corn may be selling below your production costs after the harvest. Financial derivatives can be used to minimize the total loss suffered by an unexpected crash. If the price of corn is trading for around $3.50/bushel and you would like to “lock-in” a price floor of $3, you could buy a put option at $3 and be safe from a possibility where the price went below $3. Since put options increase in value as the underlying asset trades below its strike price, the price at which the option is purchased, the total loss is the cost of the option. If the cost of the put option at $3 is 10 cents ($500=5000*.10) and if the production costs of corn is $1/bushel, then the minimum profit is $9500. The purpose of the above example is to highlight the utility of derivatives. Of course, the picture of a farmer’s derivatives portfolio can become increasingly more complicated when considering how to use a full suite of futures, options, swaps, etc. Yet, a basic intuition can be gleamed: markets and prices reflect uncertainty/risk and derivatives exist as products to minimize such uncertainty. With this understanding of derivatives, the price of any derivative takes on a special consideration. For, the derivative’s instrumentality is premised upon its ability to represent an actual hedge against the uncertainty of the underlying asset. In the above example, if the price of the put option was $2, instead of 10 cents, and corn was trading at $3.50, the state of the options market can tell you a number of things about the broader corn market. First, if the option is accurately priced and not the result of some egregious error, then the Black-Scholes model would calculate that the volatility of corn prices is a little over 200% ( ). Such volatility would be extraordinary for the agricultural market and may change your assumptions about what price you would be willing to sell your corn. Second, if your assumptions remain unchanged, buying a put option for $2 would substantially reduce your profit potential and may result in a total loss if the price of corn fell to $3 because of fees. Third, if your assumptions do change and the implied volatility of corn prices is to be believed, producing 1 bushel of corn for $1 becomes risky because there’s a substantially higher probability of corn trading below your costs. Thus, determining the validity of a given option’s price is critically important because the option’s price implies crucial aspects of the underlying market. see notes Black-Scholes When it comes to determining the value of an options contract, the process is fairly mechanical. The pervasive Black-Scholes model for options pricing is used to give investors an analytical framework for determining the value of an options contract. The Black-Scholes model is also used by investors and exchanges alike to determine “the greeks,” or partial derivatives such as an option’s or portfolio’s delta, vega, theta, gamma, etc. These partial derivatives have been very useful for risk management as well as prescribed risk-limits created by exchanges/brokerages because they determine how sensitive an option’s or portfolio’s (or another partial derivative) value is to certain parameters. An example of this is when Deribit, a large crypto derivatives exchange, liquidates risky positions; the . In the broader context of the derivatives market, when the Chicago Board Options Exchange launched its first “Autoquote” system in 1986, a program that gave traders updated prices of options being traded, it used Black-Scholes ( , 169). It’s not an overstatement to propose that the Black-Scholes model was a “ ” in the context of modern finance’s growth and the accelerating influence derivatives have in financial markets. risk engine tries to create a “delta-neutral” position MacKenzie vital contribution Such accelerating influence has also been seen in crypto markets. With the recent announcements from bitcoin derivatives exchange and testing physically-settled bitcoin derivatives to the ongoing development of Bakkt and ErisX, a lot of interest has been generated in offering US customers exposure to crypto derivatives. As for options, only LedgerX and Seed CX currently offer trading for US customers. LedgerX Seed CX The news of so many new derivatives exchanges possibly going live in the near future prompts the question: how well does the Black-Scholes model lend itself to the risk management of bitcoin investments? Certainly, the Black-Scholes model is not without its flaws, which will be taken up below. Yet, the model remains as and is attractive because it provides an easy to implement system to track risk. standard curriculum for future investment bankers A crucial feature of Black-Scholes is the implicit assumption that asset are normally distributed. By assuming a normal distribution of returns, Black-Scholes offers a framework for predicting the probabilities of certain returns that investors can factor into their hedging strategies. In their original paper, “The Pricing of Options and Corporate Liabilities,” Black and Scholes state this assumption as “[t]he stock price follows a random walk in continuous time with a variance rate proportional to the square of the stock price. Thus the distribution of possible stock prices at the end of any finite interval is log-normal. The variance rate of the return on the stock is constant” ( , 640). This assumption can be illuminated by looking at the formula. The Black-Scholes formula is: returns Black and Scholes Where: and, The inputs for the formula are: = Call option price C = Stock/underlying asset price So = Strike price X σ = volatility = continuously compounded risk-free interest rate r = continuously compounded dividend yield q = time to expiration (% of year). t = exponential term e The N(x) function is the standard normal cumulative distribution function. The N(x) function represents the probability “weighting” for the “value” part of the formula ( ) and the “cost” part ( ). In the original conception of the formula, the “value” part was denoted as the stock price times the N(x) function. This was changed later by Robert Merton, who greatly expanded the Black-Scholes model, to account for dividends. So e-qt X e-rt Roughly speaking, the Black-Scholes formula represents an investor’s return ( ) minus the cost of the option. The ‘ ’ accounts for the risk-free interest rate, compounded continuously, from the time of purchase to the expiration of the option. Essentially, the ‘ ’ represents the “time value of money” and it discounts the strike price ( ) to present value. This is done because, ideally, the option’s value should be greater than the current risk-free rate of a Treasury bill (T-bill) or government bond. If an investor could achieve a higher return by buying a T-bill, buying the option would make little sense. So e-qt e-rt e-rt X Figure 1: Log-normal distribution (left) vs Normal distribution (right). Importantly, Black-Scholes uses a log-normal distribution for options prices. However, the at expiration ((ln( / )+ ) are normally distributed. This means that the distribution of prices is skewed so that the mean, median, and mode are different. Since a log-normal distribution has a lower bound of 0, it intuitively makes sense that prices are log-normally distributed because asset prices cannot be negative. returns So X t The term ‘σ’ represents the asset’s daily volatility. When the growth term (ln( / )+ ) is divided by the standard deviation of the asset’s daily volatility (σ√ ) the distribution becomes a normal distribution. With returns being normally distributed, the volatility of an asset (σ√ ) will determine the curve of the distribution when weighted by the N(x) function. Because volatility is weighted by the N(x), the higher the value is for (σ √ ), the “flatter” the curve will be. So X t t t t Figure 2: Strike price probabilities When the N(x) function is N(d1), the function represents the probability of how far into the money the option will be if, and only if, the asset price is above the strike price at expiration. In other words, N(d1) gives the expected value, at time , of the asset price ( ) and counts asset prices less than the strike price as 0. When looking at Figure 2, if ' ' represents a strike price, N(d1) gives the expected value of the option when the asset price is to the right of the ‘ .’ When the asset price is to the left of ‘ ,’ N(d1) treats the price as 0. This represents how an option works. In the case of a call option, assume that ‘ ’ in Figure 2 denotes a strike price. A call option is a bet that the underlying asset’s price will be above the strike price at the time of expiration. If the price, at expiration, is below the strike price, the call option’s value is 0. Alternatively, if ‘ ’ denotes the strike price for a put option and the underlying asset’s price expires to the right of ‘ ,’ the put option’s value is 0. t So a a a a a a N(d2), on the other hand, is “the probability that a call option will be exercised in a risk-neutral world” ( , 335). Assuming again that the ‘ ’ in Figure 2 denotes a strike price, N(d2) represents the probability of the asset’s price being above (for a call option) or below (for a put) ‘ ’ at expiration. Because the total area under a normal distribution curve, e.g. Figure 2, represents all probabilities of an event occurring, and returns are modeled as a normal distribution, Black-Scholes models the total probability of what the future rate of return for an asset will be. N(d2) is the means of determining the probability of whether the price of an asset will be above or below a given strike by modeling the probabilities of an asset’s rate of growth. These probabilities are calculated by determining how many standard deviations away the rate of growth, from the stock price to the strike price, is from the expected rate of growth ( -(σ²/2)). Putting it all together, because the option is only paid if the asset’s price is greater than the strike (for a call) and the probability of this happening is N(d2), the expected payoff for that option in a risk-neutral world is: Hull a a r Volatility ‘σ’ is the most deterministic input for Black-Scholes because higher volatility means that the area of the normal distribution curve will be greater. This also means that the option will be priced higher because ( ) is multiplied by the N(x) function. Thus, option prices can be conceived of as merely probability distributions. If volatility is very stable and there’s a 100% chance that a stock will expire above or below a call or put option’s strike, respectively, then that option is not very valuable. Indeed, the option is useless from a hedging perspective because there’s no risk. Alternatively, if there’s a 50% chance of the stock expiring above or below an option’s strike, that option has value because it’s attractive to investors seeking to reduce the risk of holding the underlying stock. So e-qt The Fantasy of Black-Scholes Black-Scholes is by no means perfect. In part, the utility of the Black-Scholes model is hampered by its assumptions about the market. Namely, the model assumes that volatility is not only constant, but also knowable in advance. This assumption is problematic because volatility, itself, can be volatile. The Chicago Board Options Exchange created the Volatility Index (VIX) to tract the 30-day implied volatility of the S&P 500 index options. In 2018 the VIX reached a low of almost 8.5% and a high of over 46%. Volatility is by no means consistent. Moreover, finding volatility is not as straightforward as simply looking up a stock price. Whereas the stock price, the strike price, the risk-free interest rate, the dividend yield, and the time till expiration are all observable, volatility is . Volatility must be calculated by looking backwards and projecting that at time it can be known, or at least cautiously relied on. implied t Black-Scholes also suffers because the market has changed. When the market flash crashed in 1987, an important aspect of the derivatives market was dramatically affected. This was the “volatility smile.” Prior to 1987, implied volatility (IV) for out-of-the-money puts and out-of-the-money calls were almost similar in value. The market priced in unbiased IVs for both calls and puts. However, as shown in Figure 3, this changed after 1987 and the market currently tends to give higher IVs to put options over calls. The volatility smile now demonstrates “skewness.” Figure 3: . CBOE Skew Index Skew can represent in the market. If put options are pricing in much higher IVs than calls, it can be interpreted that traders are disproportionately hedging for downside risk. In the case of Figure 3, the graph suggests that there is for the S&P 500. Negative skewness indicates that there’s higher probability for values to the left of the mean. Ever since 1987, the market has priced in such skew by valuing the IV for puts higher than calls. Simply put, traders fear a future crash and have a higher demand for this type of hedging. While Black-Scholes, through a normal distribution curve, gives equal probabilities at both ends of the curve, actual markets tend to betray a more pessimistic outlook. Interestingly though, bitcoin traders are much more optimistic. the fear negative skewness Figure 4: Deribit Bitcoin Options Chain for Dec. 27th. Figure 4 shows the options chain on Deribit (the market of listed options) for bitcoin with a December 27th, 2019 expiration. It can be seen that similarly distanced strikes (7000 and 15000) from the current price of bitcoin ( ~10000) show very different IVs. Whereas the put options (on the right side) being bought at 7000 have an IV of 86.6%, the call options (on the left side) at 15000 have a slightly higher IV of 91.8%. As a result, the out-of-the-money puts are valued far less than out-of-the-money calls. Although this one option chain isn’t indicative of the entire bitcoin options market, it shows that there’s a sizable amount of speculators/investors who are undervaluing downside risk. In these respects, the Black-Scholes model should not be held as sacred. Rather, a good bit of skepticism should be applied when using Black-Scholes to price options. However, Black-Scholes, as noted above, is still widely used and certainly has its uses. Particularly, it’s useful when trying to get an idea of option prices for many assets quickly. In many respects, this easy-to-apply model may have led to s , but fantasy can still serve a purpose. ome over-reliance for many firms Kurtosis and Unpredictability Kurtosis is a measure of “ ,” or how well the tails of a sample’s distribution fit into the bell-curve of a normal distribution. Since January 2016 bitcoin has had excessive kurtosis. The formula for is: tailedness sample excess kurtosis The inputs are: = random variable X = sample size n = sample standard deviation s Kurtosis is defined as the fourth standardized central moment, and is represented as: For calculating the kurtosis of a distribution of an asset’s returns, the deviation from the mean (the difference between each random variable and the average of all values) for each daily return is needed. This deviation can be represented as: X describe the shape of distributions. Generally speaking, the first and second moments represent the mean and variance, respectively, of a distribution. The third moment represents skewness. As introduced above, skewness is the shift in the distribution away from the mean of a normal distribution. The fourth moment, when standardized, is kurtosis and changes the curve of a normal distribution in different ways. The fourth moment can be represented as: Statistical moments Since Kurtosis is the fourth central moment, the fourth moment must be normalized. Normalization can be achieved by dividing by the sample standard deviation. Thus, the fourth moment is divided by ‘ ’ in the formula above. A normal distribution has a kurtosis of 3. If the kurtosis for a distribution is higher than 3, it is called “leptokurtic.” When kurtosis is less than 3, it is called “playkurtic.” When calculating for excess kurtosis, the formula is adjusted to subtract 3 for a sample. standardized s⁴ Whereas playkurtic distributions have more uniform distributions and can have a flatter curve, “leptokurtic distributions have the property that small and large values around the mean are more likely than for a normal distribution, while intermediate changes are less likely; that is, the probability from the shoulders is moved to the centre and tails” ( , 4). As can be seen in Figure 5, a leptokurtic distribution shows very high probabilities around the mean and much higher probabilities at the tails when compared to a normal distribution. This means that, for assets, they are generally less predictable because the probabilities are skewed by giving higher probabilities to very dramatic swings in price. Thus, when an asset shows excess kurtosis, the inherent risk of holding the asset is greater. McAlevey and Stent Figure 5: A leptokurtic distribution more peaked and having fatter tails than a normal distribution of the same variance. (McAlevey and Stent, 5). When thinking about risk, kurtosis can be especially helpful. Disregarding fundamental assumptions like 'random walk' for the moment, finding the kurtosis of returns for any given time-frame can give investors a picture of how volatility is distributed. Finding out whether returns are actually normally distributed or not then adds nuance to how and when assets are considered risky. A simply focuses on volatility. The more volatile an asset is, the more risk. Conversely the more stable an asset is, the safer. However, this dualism of volatile/risky and stable/safe brushes over the nature of volatility and lumps even normally distributed returns that have a very wide curve into the "risky" category. Yet, if returns are normally distributed, then the probabilities for those returns are knowable - no matter how wide the curve is. For example, imagine an asset where the edges of the normally distributed returns reach -50% and 50%. Such an asset would be considered very volatile. But if the asset follows a normal distribution, it can be known that the tails and edges of the curve represent 2 and 3 standard deviations from the mean, while somewhere in the shoulders of the curve represents 1 standard deviation. When that information is known, an investment strategy can be tailored around such probabilities and even very volatile assets can be traded just like less volatile ones. Therefore, instead of treating risk and volatility as parallel to each other, they should be related . This orthogonal relation can produce a Volatility-Risk compass. common interpretation of risk orthogonally Figure 6: Orthogonal compass. In Figure 6, imagine that the Unpredictable-Predictable axis relates to price and the Knowable-Unknowable axis relates to probability distributions of returns. In the two bottom quadrants the prices of an asset are predictable, while in the two top quadrants prices are unpredictable. Likewise, in the two left-side quadrants the probability distributions of returns are knowable, while in the two right-side quadrants the probabilities are unknowable (or at least unreliable). In this picture, the top quadrants represent 'random walk' and the left-side quadrants represent normally distributed returns. So then, in Figure 7, the "ideal" asset in the Black-Scholes model is represented in the top left quadrant. Such an asset follows a 'random walk' and its prices are unpredictable. However, the returns are normally distributed and thus the probabilities are knowable. Alternatively, the bottom right quadrant represents the antitheses of the Black-Scholes model. The price of the asset in the bottom right quadrant is predictable but the probability distributions are essentially unknowable. This asset can be thought of as being manipulated. Either through insider trading or universal acceptance of a prescribed technical analysis, the price is perfectly predictable but the asset moves erratically. There's no uniform logic to how the returns are distributed. Instead, price action, the asset's price plotted over time, is perfectly determinative and trying to divine probabilities of returns is irrelevant. For the bottom left quadrant, the price is predictable and the probabilities are knowable. Such an asset could be thought of as a "stablecoin" where there shouldn't be any deviations in price and thus the probabilities of future returns are knowable because there won't be daily changes. Finally, the top right quadrant shows an asset that presumably follows a 'random walk' but the distribution of returns are not normal. Figure 7: Volatility-Risk compass. With the Volatility-Risk compass, a clearer picture can be drawn to determine when an asset is risky. In this sense, kurtosis can be used to indicate which quadrant an asset falls into. The kurtosis of an asset quantifies its options' risk because excess kurtosis means that the probabilities priced in by the Black-Scholes model are less reliable. Furthermore, finding the kurtosis of assets held in a portfolio can provide a more accurate measurement of that portfolio's value when looking at 'risk-adjusted returns.' This is because kurtosis will indicate the 'tail risk' of a portfolio. By identifying 'tail risk' and not just volatility, investors can gain a better understanding of the risk present in their portfolios. Therefore, when trying to account for the risk present in bitcoin, focusing on bitcoin's volatility is not sufficient. It's important to test how the volatility is distributed. If returns are normally distributed, then accurate prices for bitcoin options can be given and risk can be quantified. If returns are not normally distributed, then the probabilities of returns, reflected in option prices, are much less reliable. Bitcoin’s Kurtosis By looking at the daily returns for bitcoin from 2016 to August, 2019, taken from coinmarketcap, excess kurtosis can be found. Figure 8: 2016 Daily Bitcoin Returns (Left), 2017 Returns (Center), 2018 Returns (Right). Figure 8 shows the distribution of 2016, 2017, and 2018 daily returns for bitcoin overlaid with a normal distribution curve for those same returns. As is clear from the charts, bitcoin does not follow a normal distribution. Rather, comparing Figure 8 with Figure 5, it can be seen that bitcoin looks more similar to a leptokurtic distribution. This observation is confirmed when calculating the excess kurtosis for 2016, 2017, and 2018, with the results being 10.03, 3.29, and 2.05. The range in each chart is from -20.00% to 20.00% daily returns. For 2017, there were two observations that fell outside of this range. These values were actually 22% in daily returns. 2017 was a particularly volatile year for bitcoin and there were observations at both of the edges of the range. Volatility slightly dropped in 2018, but significant ‘tail risk’ was still present. Notably, 2018 saw more extreme volatility to the downside. Figure 9: 2019 Daily Bitcoin Returns So far, in 2019, bitcoin’s kurtosis has not subsided. Rather, there is a slight uptick in 2019 compared to 2018 with excess kurtosis being 3.92. While there is far greater probability of daily returns being close to the mean for 2019, the probabilities for the tails are relatively evenly distributed. This shows a classic leptokurtic distribution, where there is a sharp drop off from the mean and “fatter” or more even distributions in the tails. Figure 10: 2016–2019 Excess Kurtosis for Bitcoin Overall the excess kurtosis shows that probabilities for bitcoin’s daily returns are skewed to overrepresent the mean and tails from what should be expected when using the Black-Scholes model. This can be troublesome when pricing options because implied volatility becomes less reliable. Instead of volatility being normally distributed, and thus giving outsized moves greater than 2 standard deviations very low probabilities, excess kurtosis means that very large changes in price are less predictable. As a result, an asset may show relatively low volatility, and subsequently give very low probabilities to large changes in price, but such volatility is not truly indicative of how volatile an asset can be. Looking back to the Volatility-Risk compass in Figure 7, bitcoin is likely represented in the top right quadrant. Presumably, bitcoin's price is unpredictable and random. However, the probabilities of returns do not follow a normal distribution. Comparisons and Conclusion Thus far, it has been shown that bitcoin exhibits excess kurtosis. So is bitcoin an outlier when compared to the broader stock market? Yes, and no. Excess kurtosis is by no means only germane to bitcoin. Plenty of assets exhibit excess kurtosis, even indexes like the S&P 500. In 2018, the S&P 500 had an excess kurtosis equal to 3.09. While this is lower than bitcoin’s 2016, 2017, and 2019 excess kurtosis, it’s actually higher than bitcoin’s 2018’s kurtosis. Of course, 2018 was a very volatile year for the S&P 500. At the beginning and end of 2018, there were sharp declines in price and very aggressive price rallies. In fact, for 2018, the S&P 500 saw the largest spike in the one-year rolling kurtosis that has been observed in almost 30 years. As Figure 11 shows, the beginning of 2018 represented relatively extreme kurtosis when the index suddenly fell >10%. However, Figure 11 also shows that, give or take a few spikes, excess kurtosis has been low since 1991. Figure 11: One-year rolling kurtosis S&P500. Source: . Financial Times A histogram of the S&P 500’s daily returns for 2018 show a distribution much closer to a normal distribution when compared to bitcoin. In Figure 12, excess kurtosis is clearly present because there are many days where the returns are well outside a normal distribution curve. Yet, for the 250 observations of daily returns in 2018 for the S&P 500, only 6 fall outside the normal distribution curve. In 2017, for the 364 observations of daily returns for bitcoin (bitcoin trades everyday of the year and observations of returns begin Jan, 02), 28 fell outside of the normal distribution curve. In this respect, when only focusing on instances that fall outside the tails of the normal distribution curve, S&P 500 presented a lower chance of experiencing extreme, and hence unpredictable, price swings. Figure 12: 2018 Daily S&P 500 Returns What can be taken away from these findings? While it’s certainly true that the S&P 500 does not fall into a normal distribution curve, it is also true that it fits a normal distribution better than bitcoin. Why this is can only be left to speculation at this point. I believe that there can be at least three possible reasons posited. First, bitcoin represents a different asset class and follows different assumptions from the broader market. Second, bitcoin, at this time, is an immature market and will be tamed by institutional investment. Or third, the Black-Scholes model is becoming less reliable overall and volatility, as well as unpredictable distributions of such volatility, will become the ‘new normal.’ Regardless of which one of these reasons is true, it must be concluded that bitcoin options are likely mis-priced and ‘delta-hedged’ bitcoin portfolios are not valued accurately. This can be problematic, especially in the context of many new crypto derivatives exchanges coming to the market, because the relatively high implied volatility of bitcoin does not tell the whole story. Lurking behind such volatility is excess kurtosis, and as a result an investor’s ability to hedge away risk is greatly reduced. Notes From Brenner’s and Subrahmanyan’s “A Simple Formula To Compute Implied Standard Deviation” we can derive from Black-Scholes: Where: = Option price C = Current stock price S = Time until expiration T = volatility σ In the corn example, the option price was $2 and the current price of corn was $3.50 and assume that option contract is for 6 months, or .5 years. It should be noted that this formula is for deriving volatility from a option’s price. The example used a put option. As a result, the volatility given will be slightly inaccurate. Yet, for simplicity, and because this is a tangent anyways, I’m going to treat the option as a call option. call Using the equation above: σ = √(2 π/.5)*(2/3.5) σ = 202.73% Brenner, Menachem and Marti Subrahmanyan, “ ” 44(5) (1988). 81 A Simple Formula to Compute the Implied Standard Deviation. Financial Analysts Journal Resources Black, Fischer & Myron Scholes. “The Pricing of Options and Corporate Liabilities.” 81(3) (1973). Journal of Political Economy Fama, Eugene F. “Efficient Capital Markets: A review of Theory and Empirical Work.” 25(2) (1970). The Journal of Finance Hull, John C. . Tenth Edition. New York: Pearson Education, (2018). Options, Futures, and Other Derivatives MacKenzie, Donald. Cambridge, MA: MIT Press, 2006. An Engine, Not a Camera. McAlevey, Lynn G. and Alan F. Stent. “Kurtosis: a Forgotten Moment.” 49(1) (2017). International Journal of Mathematical Education in Science and Technology Malkiel, Burton G. “The Efficient Market Hypothesis and Its Critics.” 17(1) (2003). Journal of Economic Perspectives Westfall, Peter H. “Kurtosis as Peakedness, 1905–2014. ” 68(3) (2014). R.I.P. Am Stat