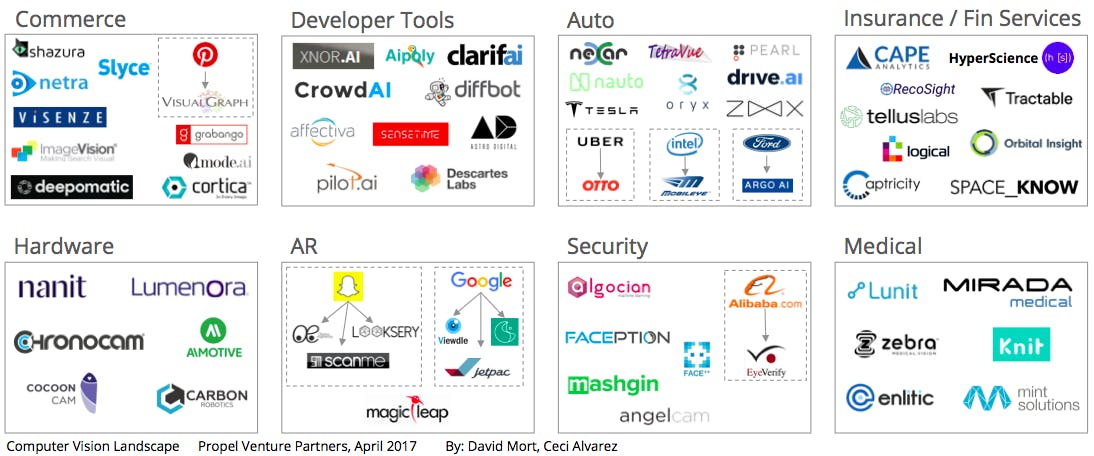

recently celebrated its one year anniversary, with our first annual Summit taking place in April. At the Summit, I had the opportunity to share some thoughts on computer vision, and its impact on financial services. Propel Venture Partners Impact on Financial Services Computer vision in financial services will serve as an enabling more so than a disruptive technology. While financial services players will develop an understanding of computer vision, they will not be uprooted by computer vision startups, and instead will be buying their software. Compared to other trends more central to the wave of the last five years, computer vision has a clearer value proposition for early adopters. technology fintech Broadly speaking, the digitization of the world around us through the camera lens will lead to better user experience (UX), with more pre-populated fields, automatically accessed and input through computational means. In addition to better UX, the associated process automation through extracting information from documents has the ability to accelerate internal efficiencies, and redefine workforces. Insurance Computer vision technologies will have a large impact on insurance carriers. For starters, carriers will benefit from better UX due to pre-populated fields leveraging information extracted from imagery. The larger impact will be derived from more precise underwriting, with policies priced to the exact specifications, quality, and granular risk. For carriers that are slow to adopt computer vision technologies, they may be underwriting high-risk or fraudulent policies without knowing. Additionally, as these carriers are unable to assess granular risk, their best customers will leave for carriers that can price across a more precise risk curve, as the cost of insurance will go down for the lowest risk customers. This could leave slow moving carriers with a high-risk book of business, without the tools to assess the risk they retain. Additionally, insurance carriers are likely to feel the full force of computer vision hitting the automotive market, driven by the adoption of autonomous vehicles. Over the next decade, drivers without semi-autonomous features may be priced out of the auto insurance market, as their risk levels go beyond the appetite of traditional carriers. For carriers that are slow to react, they could be left with an entire book of high-risk polices, as anyone left in control on the road becomes the equivalent of non-standard auto risk. Lastly, computer vision could reduce the need for human inspectors, while providing more accurate and real-time data. Some computer vision applications can even reconstruct crashes and measure severity by utilizing the camera and accelerometer from a smartphone. Capital Markets With advances in geospatial data and computer vision technologies, we are able to track activity on earth at vast and granular levels, to an extent that has never been possible. With technologies commercially available today, investors, economists, and governments can track activity such as US retail traffic, down to the retailer, by tracking automotive activity in parking lots. Hedge funds use this data to get a leg up on retail patterns, global water reserves, world oil storage, poverty mapping, and country-level economic indexing. Commerce Commerce giant Amazon is an early leader in commercializing computer vision, with applications in the wild, most notably at the AmazonGo store near the company’s headquarters. AmazonGo is an alpha version of a quick service physical retail store, which opened in 2017. The store has no registers for checkout, and instead consumers simply walk in, grab what they want, and walk out. Amazon began working on the AmazonGo concept store over four years ago, as a way to “push the boundaries of computer vision and machine learning to create a store where customers could simply take what they want and go”. AmazonGo relies on “computer vision, deep learning algorithms, and sensor fusion, much like you’d find in self-driving cars”. [4] It’s too early to know the full impact of AmazonGo on physical retail, however, convenience will play a large role in wherever consumers elect to shop. With this in mind, traditional retail must be ready to arm their stores with computer vision technologies. It’s a greenfield opportunity for technology providers. Another notable application for computer vision in commerce is for identifying and verifying goods on a marketplace. Commerce players such as Pinterest and Amazon are already using computer vision to help consumers discover new products, or predict consumer-buying behavior. For verification, computer vision plays an important role in identifying fraudulent products and listings. Marketplaces use these technologies to identify fraudulent listings, analyzing millions of images to find duplicate listings, or photos found elsewhere. Banking The lowest hanging fruit at banks exists in the back office, specifically compliance, accounts payable, underwriting, and the branch networks. Within compliance, computer vision will transform Know Your Customer (KYC) processes, which is already happening in Europe at banks such as BBVA, where customers can open an account via a mobile phone with a selfie and video call. Instead of relying solely on databases with duplicate names and dates of birth, with computer vision, banks can more distinctly identify with whom they are doing business. In the back office, where significant paperwork is present, computer vision will improve accuracy, increase throughput, and reduce the amount of time required to do tasks. In the branch networks, computer vision technologies may monitor customer emotions and deliver customer insights to drive improvements over time. [5] In March 2017, Wells Fargo announced that all 13,000 of their ATMs would work without debit cards, replaced by codes generated on a smartphone. The decision was in part to combat card fraud, which has steadily increased. We believe the move to smartphone codes is a bridge to computer vision, where no smartphone code would be necessary. In this case, using only our faces and behavioral characteristics, banks will authorize transactions. In other examples, Visa may learn to incorporate contextual information from computer vision at the point of sale for risk models. Leveraging computer vision technologies, banks are in a better position to track and value assets with a higher degree of certainty. Real estate portfolios can be monitored more effectively, broker price opinions could be streamlined, and project financing could gain intelligence. Related to commerce, mobile wallets will be key to a checkoutless experience. Card networks such as Visa and MasterCard will benefit, however it is less clear the role banks will play. Lastly, the second largest consumer purchase behind the home, the automobile, will impact financial services, as with autonomy will come changes to ownership and financing models. Conclusion Computer vision is emerging as a ubiquitous input, with commercial grade technologies beginning to reach the market. The digitization of the world, pushed forward by computer vision, creates enormous opportunities in the financial services ecosystem. The impact is material to insurance, capital markets, commerce, and banking, however the role of computer vision has a larger economic impact, saving businesses and consumers money, and making processes more efficient. Early adopters of computer vision will prevail. If you are an entrepreneur building computer vision technology relevant to financial services, let’s connect. Thanks to Ana-Cecilia Alvarez for helping with this post and Propel’s computer vision research. Propel Venture Partners is an early stage venture capital firm founded in 2016 focused on the intersection of technology and financial services. The investment team is based in San Francisco and invests globally in entrepreneurs rethinking and rebuilding financial services.