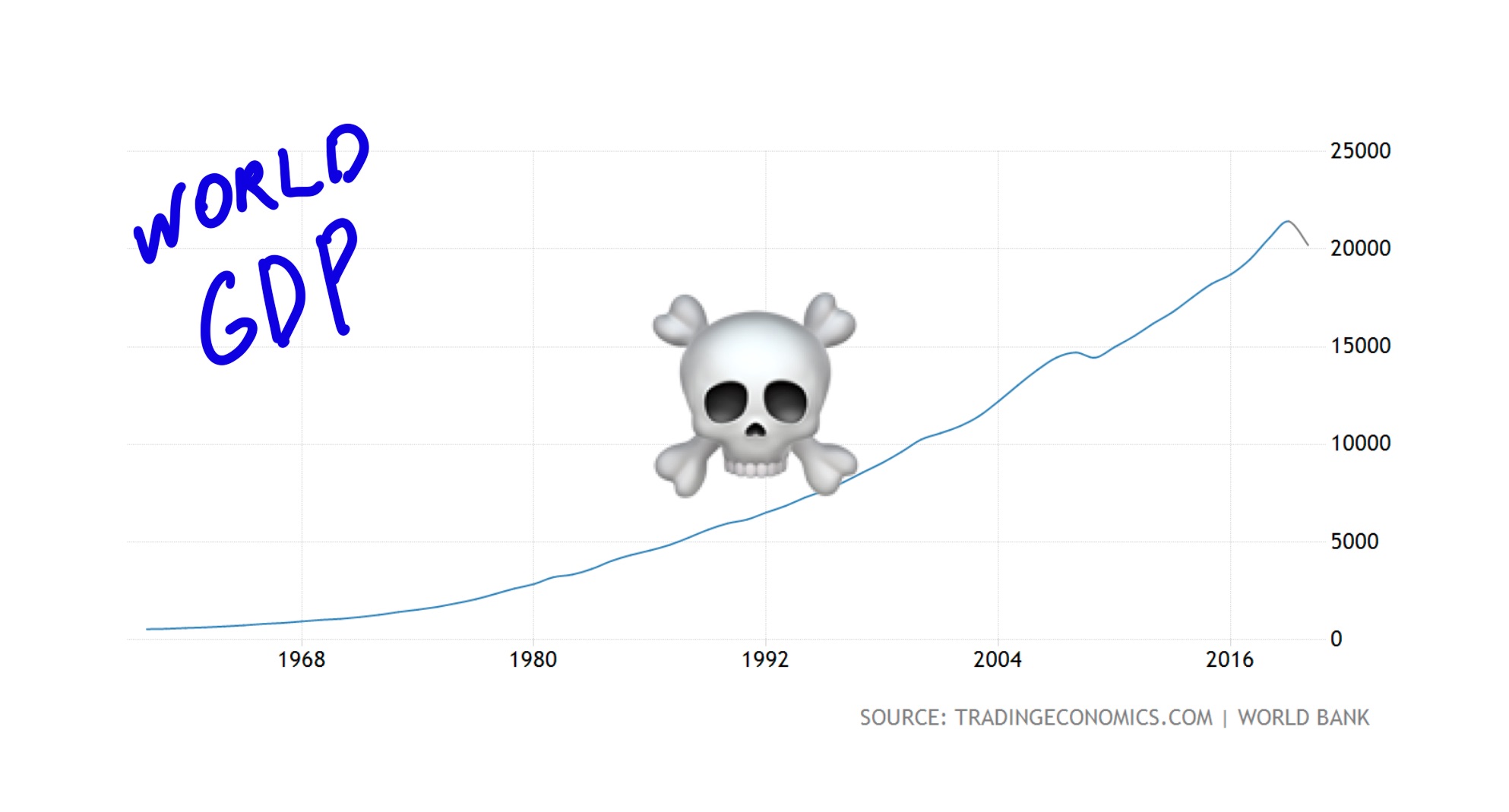

During the 2007 crisis, I was 15 years old, obviously too young, to understand what's happening. My father was upset. He tried to explain to me that it's the crisis that has come, and we will have to cut expenses and save. The central mystery of the crises for me was that somehow, has less money now. It's like some umount of money magically disappeared. So I naturally asked my father: but if everybody has less money, somebody has to have way more now? everybody In this series of articles, I try to understand the answer to this question and explain my views on why we are facing crises, why money disappears, and why we are on the verge of fundamental changes. You can ask me a question, but why do I need to know the answers? You don't. But if you know, next time while drinking with your buddies, you will be able to make them look stupid and score the girl who is way out of your league. How is growth calculated? Before stating that growth is dead, let's figure out how to measure it. The most common measure politicians and economists use is GPD. Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country's borders in a specific time period. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country's economic health. -- Investopedia But you will be right to note that the can of cola costs now considerably more than ten years ago. No wonder we have growth in monetary value. Smart economists thought about it and introduced Real GDP. It's GDP adjusted for inflation and often called "constant dollar" GDP. Politicians use rarely use real GDP in their public speeches and announcements though, spoiler alert, because it's really lower. For my nerdier (more educated) readers, there is another cool concept - ( ), also called , which is usually measured as the ratio of aggregate output (e.g., GDP) to aggregate inputs. But we are going to talk about productivity and money printing in the second part of this series. total-factor productivity TFP multi-factor productivity So, what's up with growth? Honestly, when I started to research for this piece, I was surprised by how scattered and uncomplete a lot of data is. But it makes sense. First of all, growth is an ideology, and it's not cool to put proof of it's failing on the front page of Google (that's for my conspirologists friends). Secondly, data is going all the way to the early 1900s, when the data collecting process wasn't as great as now. And don't forget who we are dealing with here, we try to understand economists, and they have a bit different view on the world. I want to earn money, so my friends and I can have a sweet life. Economists want to save the world using math, not the most productive way to do real stuff. So it's super easy to find tons of exciting and complicated models, but hard to find specific and actionable conclusions. But let's focus on some more straightforward concepts. U.S. GDP & Real GDP Here we can see the growth of GDP, and it is pretty easy to see a beautiful downward trend. GDP though has a lot of criticism that it's not reflecting people's quality of life. U.S. Hourly Labor Productivity and Hourly Real Wage Growth: Total Economy, 1948–2015 I think the hourly rate is a pretty good measurement of people's wellbeing, and the trend is very similar. BUT, these are the U.S. charts, and Amerca is a developed country, it makes sense for the growth to slow down. Do workers whos real wage is decreasing care about it? But let's see another chart, maybe developing economies are fuelling the growth. Global GDP growth is slowing down as well, but what is that red dotted line over there? Reasons why it's slowing down. It turns out that the red line is population growth. The world's population is currently growing at a rate of around per year (down from 1.08% in 2019, 1.10% in 2018, and 1.12% in 2017). 1.05% The annual growth rate reached its peak in the late 1960s when it was at around 2%. The rate of increase has nearly halved since then and will continue to decline in the coming years. Prof Hans Rosling, in his book Fuctfullnes, estimated that due to the number of countries moving from "developing" to "developed" and an overall increase in quality of life, the fertility rate should drop across the board and population should stabilize at around 11-12 billion people. While the book sparked a lot of debate, I have a feeling of "fact picking" after reading it. Nevertheless, I tend to agree with his view on population growth. To dive deeper into sources of growth, Peter Thiel highlights two of them: Extensive An increase in market size. Here we talk about population growth, increasing global trade, new market discovery. Most of these drivers are already exhausted, and lately, we see deglobalization trends, powered with U.S. and China trade wars. Intensive New technologies and better tech. But the real increase in productivity was less than anticipated. Yes, the internet played a huge role in market expansion, but we haven't seen a technological revolution in a while now. The first iPhone was launched in 2007, and while you can't argue that today's iPhone is much, much better, it is an evolutionary change. How many robots doing humans' work you see when you go somewhere? And don't forget that upgrading the existing infrastructure is expensive. I was struck by the absence of stores accepting Apple Pay in California. In Russia, even in a rural area, NFC-based payments are widely accepted. Everything because we didn't update the infrastructure we built it with new tech from the get-go. Centralization Over the period from 2008 to 2018, based on publicly available information, Google has acquired 168 companies, Facebook has acquired 71 companies and Amazon has acquired 60 companies. Totaling to 299 acquisitions. Despite the topic being well discovered theoretically, there is surprisingly little systematic evidence to date. An exception is a recent paper by Cunningham, Ederer and Ma (2018) that looks at acquisitions in the pharma industry. Their overall estimates indicate that 6.4% of all acquisitions in the market are killer acquisitions. This M&A activity is viewed by many as a power halting innovation. Recent Senate hearings are the confirmation. Is "entry-for-buyout" pro- or anti- competitive? The "efficiency effect" obviously suggests that allowing buyouts of potential entrants stimulates innovation. Also, Rasmusen (1988) argues that, on the plus side, the possibility of buying out entrants limits the scope for inefficient entry deterrence strategies. However, because the threat to incumbents is higher when the entrant's product is a close substitute to the incumbent's, then entrants will invest in duplicative innovation, which is socially wasteful since it does not lead to new products or lower prices. Ex-post Assessment of Merger Control Decisions in Digital Markets In my opinion, we need more empirical evidence on the subject, and sure enough, we will get them soon. Where am I going with it? In this post I'm laying down the foundation for future posts. #003 Blunt Economics Part 2: Where did the money go? #004 Blunt Economics Part 3: Digital Economy #005 Blunt Economics Part 4: Change or die trying #002 Blunt Economics Part 1: Death of Growth Subscribe to get them straight into your inbox. Originally posted at my blog #002 Blunt Economics Part 1: Death of Growth