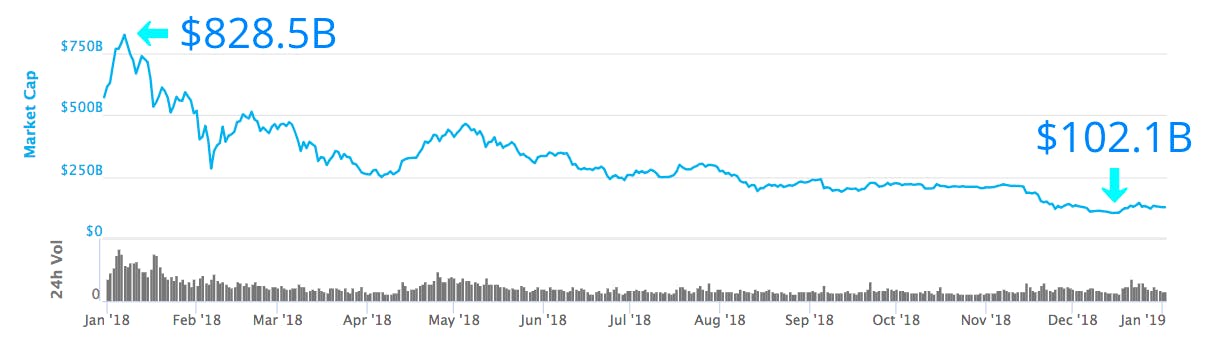

When I first heard of Bitcoin, it sounded like something out of a dystopian sci-fi novel. Digital, cryptographic, uncensorable money? It seemed such a radical idea, it couldn’t possibly belong in this decade. But if it did — if Bitcoin were to go mainstream — I was convinced it would lead to a massive geopolitical disruption, shifting the power relations between governments and their citizens. It would mean investing into Bitcoin would be like funding a revolutionary army. It would be so subversive, only a few crazy people would be willing to do it. Of course, I was wrong about every part of that. Grandmothers now own Bitcoin. And with a few notable exceptions (namely China and India), world governments have been surprisingly welcoming toward cryptocurrencies. Bitcoin is legal almost everywhere. There’s been a on the regulatory front lately. But amidst the frenetic crypto news cycle, it’s easy to lose sight of how weird it is that Bitcoin is legal at all. Obviously it’s good that it is — but we should be surprised this happened! lot of tumult Bitcoin was supposed to be the enemy of governments. It was supposed to destroy the state’s monopoly on monetary policy, it was supposed to be a battering ram against the banks and financial surveillance. Indeed, Bitcoin was supposed to erect nothing less than an uncensorable shadow financial system. So why have governments ushered Bitcoin through the front door? Three explanations I’ve been thinking about this question a lot lately, because I feel it demands answering. I’ve come up with three potential explanations. The first is that “all innovation is good innovation.” Perhaps governments recognize the inevitable growth of blockchain technology and don’t want to stem innovation too early via overregulation. This is plausible: you still hear the echoes of “blockchain not Bitcoin” within the halls of industry, and blockchain idealism has become safe cocktail party conversation. But this explanation falls short. First of all, we already blockchains. Further Bitcoin development isn’t likely to contribute to enterprise blockchain deployments. If the purpose of letting Bitcoin flourish was to usher in the age of enterprise blockchains, its job is already done. have Perhaps governments are pattern-matching blockchains with the Internet. A wait-and-see approach to internet regulation was clearly instrumental to its flourishing, and perhaps governments intend to do the same here. But governments have also fought tooth and nail against end-to-end encryption, P2P filesharing, privacy technologies like Tor, and financial networks that enable tax evasion (see and global financial surveillance policies like ). If Bitcoin threatens the power of financial surveillance, then it would be considered far more dangerous than any of these prior technologies. e-gold FATCA In light of these examples, “all innovation is good innovation” doesn’t adequately explain the lax attitudes of governments. The second possibility is that governments are too dumb to recognize Bitcoin as the snake that will eventually bite them. Governments can certainly sometimes be reactive and short-sighted. But I don’t think this one is correct. By and large, the strongest world governments are thorough and ruthless at identifying and neutralizing threats to their power. Furthermore, Bitcoin’s proponents have historically had very little political influence. Bitcoin’s past has been marred by associations with criminality, dark markets, and digital anarchy. This is precisely the kind of thing that governments would put in the “illegal internet shenanigans” bucket. Neither of these explanations are satisfying. So that leads me to the third and perhaps most radical possibility: Bitcoin is not actually a threat to sovereigns. I’ve become increasingly convinced of this. In fact, Bitcoin might just be the most sovereign-friendly cryptocurrency. Hear me out. I think there are three main reasons why this is true. Bitcoin doesn’t offer true anonymity Bitcoin is often described as an anonymous cryptocurrency, but this is incorrect. Bitcoin is actually . The distinction is crucial: under a cryptographic pseudonym, your behavior can still be tracked. pseudonymous How is this done? It starts with the fiat onramps, where an exchange collects information on you through their KYC process. This information that is often shared with other exchanges when investigating suspicious activity. Even once take your Bitcoin onto the mainnet, your activity can still be tracked. are often used to identify exchanges, mixers, and other common blockchain services you use. connect to large swathes of the Bitcoin network and correlate transactions with their originating IPs. Even with meticulous opsec and address rotation (which most people don’t do), if you ever want to turn your Bitcoin back into fiat, that offramp is just as highly regulated. Often you will be turned away if your Bitcoin appears tainted by signs of illegal activity. Heuristics and clustering analysis Supernodes This is more than hypothetical. Exchanges have significant insight into the flows of Bitcoin — enough to successfully deter hacks, stolen funds, and regularly file (as all US exchanges are required to). We saw this with the and with analysis of the . Companies like Chainalysis provide surveillance services to law enforcement and various three-letter agencies, . suspicious activity reports Mueller Probe Mt. Gox hack reportedly earning more than $5.7M in 2018 via government contracts For the average person, this is probably not a big deal. Most cryptocurrency users aren’t doing anything illegal and needn’t worry they’re being targeted for surveillance. But consider: how is this any different from other systems we use? Most people feel their cell phone conversations are private. But in the back of their heads, they know that their phones could be tapped or their phone provider subpoenaed. We take solace that this surveillance is unlikely and usually requires a significant legal threshold. And yet, we know not to be surprised if someday our phone calls are replayed before a jury of our peers. Bitcoin falls into the same security model. One could even argue that Bitcoin is less private than using an overseas banking system. The U.S. has limited insight into what happens in unfriendly banking jurisdictions. But everything on the blockchain is visible all the time. What a gift it would be to the US if every foreign financial institution made their transactions public on a blockchain! To the uncritical eye, Bitcoin’s pseudonymity looks like a radical step forward in economic privacy. But a facade of privacy is more dangerous than no privacy at all. The more safe and empowered citizens are convinced they are, the more the state is free to accrue real power over them. This is the first reason Bitcoin is sovereign-friendly. A store of value is not threatening I once believed that if Bitcoin truly succeeded, it would become a global currency. Every economy in the world would be united by their usage of Bitcoin as a new global cryptographic money. It’s become increasingly clear how unlikely this is. This is both because Bitcoin cannot be a worldwide currency, and because Bitcoin can succeed without becoming that worldwide currency. Classically, a currency must act as a medium of exchange, a unit of account, and a store of value. Bitcoin is unlikely to become a global currency for several reasons, each of which could be an essay on their own. But in short: Bitcoin has , and its divisibility is too low (currently about 3c USD for non-Segwit transactions). Furthermore, even if second-layer scaling technologies like the Lightning Network prove successful, Bitcoin’s deflationary monetary policy makes it a . too high latency, too low throughput due to the rising dust limit poor medium of exchange If it came down to it, and central banks felt a digital currency posed enough of a threat, they would happily incentivize (or mandate) usage of their own currency in order to maintain sovereign monetary policy. It’s worth remembering: money is the ultimate network effect, and it’s incredibly sticky. This is especially true in the first world. Our financial system may be built on rusty old cogs, but it has been retrofitted with so many layers of abstraction and usability that for most people most of the time, it’s good enough. Putting the two side-by-side, our current financial system is far ahead of the UX of cryptocurrencies (though I eagerly await the day that changes). So Bitcoin is not suited to be a global currency. But Bitcoin can still succeed! As Nic Carter (no affiliation with the Backstreet Boys) documents, Bitcoin has iterated its way into a Turns out, sovereigns are pretty okay with this. vision of “digital gold.” Note, Bitcoin becoming a form of digital gold is still a long ways away. To say nothing of their relative volatility, the market cap of gold is in the trillions of dollars. Bitcoin is still dwarfed by gold’s dominance as the global store of value. But sovereigns are not principally concerned with protecting the status of gold (except insofar as they hold some amount of gold in reserves). A disruption in the worldwide store of value would not be a significant threat to their power. But I’ll tell you what would be: if Bitcoin were to become a medium of exchange. Then it could support a rich on-chain economy, and its users might be able to conduct their financial lives on a parallel, uncensorable economy. But Bitcoin has proven to be a poor medium of exchange, and there are few substantial businesses built entirely on Bitcoin. As a store of value, the story is much simpler. The flow of Bitcoin usage must begin and end with fiat currencies, bottlenecked at off-chain exchanges like Coinbase or Bitfinex. These exchanges serve as chokepoints where the government’s hand can regulate on-chain activity. Any criminal activity ultimately needs access to fiat liquidity — a store of value cannot be used to finance a real-world operation. (Bitcoin is also unable to support DEXes or easily interoperate with other blockchains. This forces markets to consolidate around these off-chain exchanges.) This is provides a neat explanation for why India and China have been the two major countries to ban crypto. Both have strict capital controls and burgeoning middle classes, itching to escape the local currency. Their primary concerns are around economic protectionism and preventing capital flight. Both and also have strong restrictions on gold imports. To countries unafraid of capital flight, a store of value poses less of a threat. India China But a medium of exchange is scary to governments. is the canonical example of such a medium of exchange that attempts to circumvent the government’s monopoly on financial regulation. But a pure store of value whose onramps and offramps can be easily regulated, and which cannot steer clear from the financial-industrial complex — well, it’s less of a threat to sovereigns. They might even call it innovation. Liberty Reserve This is the second reason why sovereigns are open to Bitcoin. Bitcoin belongs to no one It might sound like this article is ragging on Bitcoin. But I’m actually very bullish on Bitcoin. Bitcoin is by far the most decentralized cryptocurrency, and it’s the only currency that can plausibly be said to be politically stateless. This is an enormous advantage in becoming a store of value. No other cryptocurrency can claim this, and it’s possible that no other currency ever will. You see, almost every other cryptocurrency that exists today can be pinpointed on a map. It was concocted by a single mind or a few minds. We know where they come from, where they live, and where they are evangelizing the project. Bitcoin is the only exception. Its pseudonymous creator, Satoshi Nakamoto, is now an apparition. Bitcoin belongs to no one, and it relies on no one. If all of its developers were rounded up and thrown into secret prisons, its development would continue under another set of names. This also implies that if a government were to throw its support behind Bitcoin, it would not cede power to any other country. This fact is under-appreciated. Bitcoin’s statelessness makes it the only cryptocurrency that has a chance of being purchased by a central bank — ultimately, the only buyer that could make Bitcoin into a trillion dollar asset. This legitimization would consolidate it as a true digital gold. Could a central bank ever buy Ether or IOTA? I suspect not. These are companies, earthly organizations with headquarters and identifiable leaders. As much as I love Ethereum, it was created by a Russian-Canadian, with a mostly American and European developer team. The founders walk around. They have plans, they change their minds. They have passports and allegiances. Ethereum is strictly of this world. Bitcoin, on the other hand, is from nowhere and everywhere: all countries can see their own reflections in Bitcoin. Americans see the Bitcoin Foundation and many Core developers as American. Japanese see Satoshi Nakamoto as one of their own, and thus Bitcoin as one of their inventions. The British claim that . The Chinese claim they control the mining industry and hardware that secures Bitcoin. Satoshi was likely of British origin I’m not criticizing Ethereum on this point! Ethereum is a fantastically innovative project, and to innovate rapidly on anything requires coordination and centralization. But Ethereum is not analogous to Bitcoin on this point, and given that it’s only a few years old, we should not expect it to be. Perhaps a decade from now things will look different, but for now Bitcoin is in a category of its own. Bitcoin is the only digital currency that resembles a global commons. These factors will make governments more likely to embrace Bitcoin as a store of value. An uneasy compromise Remember, if governments truly believed Bitcoin were a threat, they would outlaw it and shut down cryptocurrency exchanges. This would crater prices and liquidity. It would not be the end of Bitcoin of course, but it would be the end of Bitcoin’s dream of displacing gold. In a way, perhaps Bitcoin’s technological inertia and weak privacy guarantees are more adaptive than we think. Perhaps if Bitcoin were innovating as aggressively as Ethereum or Zcash, we would not be in the situation we are in today. So the question remains open: even if Bitcoin has been relegated to be a store of value, could some other cryptocurrency become a global medium of exchange? Right now I believe governments don’t see any possibility of this happening soon, which must be why they’re allowing the experiment to continue. And to be honest, the sober among us don’t either — right now the only killer app for cryptocurrencies is speculation. But as the technology matures and these systems begin to scale, this will change. Indeed, when that happens, we should expect the next phase of crypto to be messier. It won’t necessarily come with the uncritical blessings of governments. Ultimately, I don’t know the answers to these questions. To tell you the truth, I’m unsure even about these conclusions — I am not an expert on regulations nor on international politics. And in reality, governments are not animated by a single intention, but rather are complex, emergent processes composed of many factions. The last decade has lucidly taught us: governments are difficult to predict from first principles. Either way, I want to see this experiment play out. There is no doubt in my mind that the way money works 50 years from now will look nothing like it does today. The only question is what path it takes to get there. Disclaimer: These are my personal views — they do not represent MetaStable Capital, and they should not be construed as investment advice. I am not your investment adviser, I am not your lawyer, and I am not your father, even though your mother and I love each other very much. Full disclosure, I own some Bitcoin, as does MetaStable Capital.