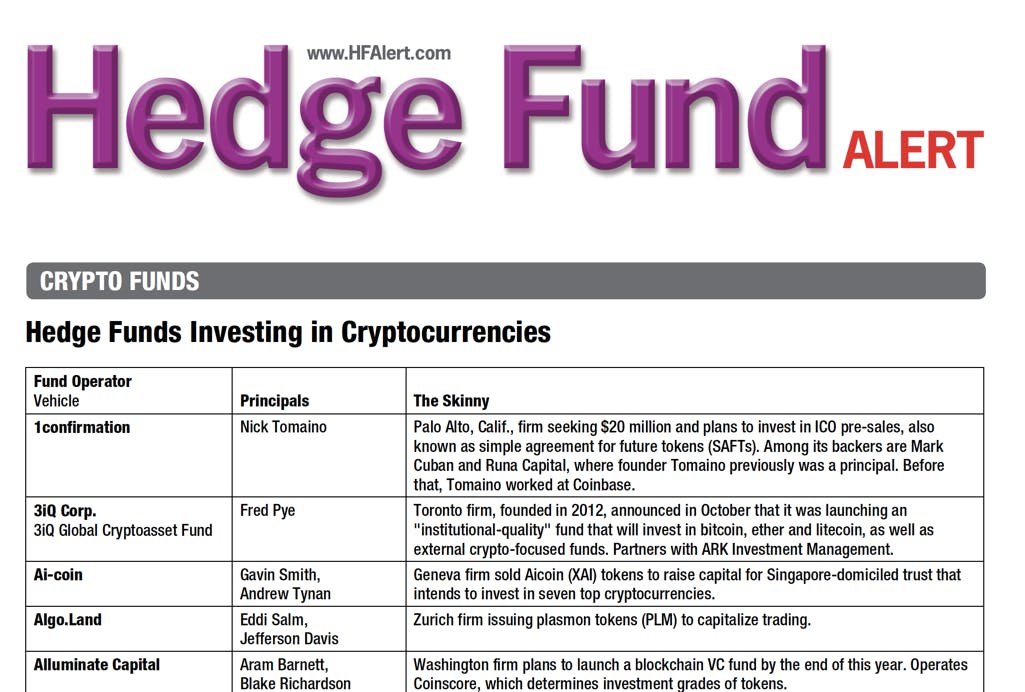

At the end of a crypto event last week, two Millennial-era entrepreneurs approached me and started chatting about their new venture. It was multi-faceted: a -enabled services business that would have a major impact on the world — but would first be funded by the raise of a crypto hedge fund. That hedge fund would invest in Tokens and ICOs — with 20–30% set aside to invest in their as-yet undeveloped crypto services business. blockchain First step in building their services business: raise money for their new hedge fund. How? A bit of savings and credit card debt, an apparent trust fund and — reluctantly — a fundraise (like them old-timers do it). At the end of a conversation, we were joined by a few other folks. One of them was a young lady whose day job is at a bank, but has a side hustle going with a new Crypto Hedge Fund based in the British Virgin Islands. This Hedge Fund was Tokenized — investments convert into a Token that will rise and fall in price based on the value of all investments in the portfolio — and was structured to raise from investors based in India. $300k had already been committed toward a $5–10M raise. Including these two, that made no less than 8 hedge fund pitches for the night. Not even close to the record. According to Hedge Fund Alert, as of November 2017 there were already 130 Crypto Hedge Funds. Many are names you might already recognize: , , , . But underground and unlisted, there are hundreds — maybe even thousands — of smaller hedge funds that are just developing. MetaStable BlockTower Multicoin Capital Polychain The majority are sub-$10M vehicles. “Training Wheel” funds that will establish credibility for something bigger later. That said, toss a rock into any crypto crowd and you’ll certainly hit someone with their sights on a $20-$50M fund. Some focus on ICOs. Some on Tokens. Some on equity or SAFTs. Some will ferret out Chinese blockchain companies that will be huge in the U.S.. Some tap into Telegram pump and dump schemes. And some…well, why pick any strategy at all? Many are raising money from family offices. A handful still focus on VCs and angels. A bunch mention the Whales they know on Reddit who might invest. One hung out with that kooky billionaire crypto maven, , but was too awe-struck to ask him for an investment. Brock Larson Leadership of these new hedge funds is remarkably inconsistent. Sure, there are experienced entrepreneurs and some with substantive financial industry skill— but most have little to no experience, save for the fact that that they have a boatload of crypto enthusiasm and can rap the blockchain lingo. Frighteningly few seem well-versed in the regulatory frameworks required for investing other people’s money. I asked one high profile crypto hedge fund manager (one that had already raised funds and had been actively trading, mind you) if he was registered as an ERA or RIA. “Neither” came the response, before noting he was actively discussing regulation and compliance with peer funds. The first hedge fund was created in 1949, by Alfred Winslow Jones, with investable assets of $100,000. Today Renaissance Technologies, one of the world’s largest hedge funds, manages north of $45b of investor capital. The term “hedge fund” is derived from the strategy of increasing gains — and offsetting losses — by hedging investments using a variety of sophisticated methods, including leverage. For traditional hedge funds, long-short strategies are often employed: invest in long positions (which means buying stocks) and short positions (which means selling stocks with borrowed money, then buying them back later when their price has, ideally, fallen). I bet if we polled all crypto “hedge” funds, less than 5% even understand leveraged buying or long-short strategies. Truly. One labeled their strategy as, “pure intuition.” But, well, the term does sound cool. hedge And probably helps a whole heck of a ton when raising money. Ok, that’s not fair. There are two obvious reasons most crypto funds label themselves as hedge funds. Unlike mutual funds, hedge funds often seek to generate returns over a specific period of time. This is called the “lockup period”. Invest in a hedge fund and you cannot get out or sell shares until the lockup is over. For those leading as investment manager, this provides ample time to stay in business while you figure everything out. Lockups. Hedge fund managers receive a percentage of returns they earn for investors. A typical 2/20 ratio means that 2% of the fund covers management fees (salaries, operations) and 20% of the returns go to the fund managers before an investor sees a dime. 20% Returns. Hey, this hedge fund thing sounds pretty good after all. So, A Few Predictions 2017 saw the rapid rise and fall of public perception of ICOs: What started as an innovative launch strategy became a misused get-rich-quick investment strategy. cryptocurrency By 2019, Crypto Hedge Funds will follow a similar pattern. Massive saturation will hit faster than anyone imagines, the cool factor will fade and capital inflows for non-sophisticated vehicles will dry up fast. Beyond that whopper, 3 additional predictions for the Crypto Hedge Fund Market: Crypto Fund Managers will become ultra-aware and over-burdened by one major painful oversight: operations. The process of buying and storing cryptocurrency is not for the light hearted. There’s managing exchanges and OTC partners, setting up digital wallets, ensuring a foolproof custody process and tracking activities. This requires focus, time, energy, patience and resources. Fantasies of patient, thoughtful investing will be obliterated by the grind of producing tax-tracking spreadsheets and digital wallet management. Expect a wave of 3rd party resources to service the funds that stay in business. The 2/20 ratio and lockups will fall out of favor. Investors will want the same democratization and flexibility that cryptocurrency itself promises. Someone sitting in the middle taking an outsized portion of returns, while holding money hostage, seems awfully, sarcastically oxymoronic. A lack of competitive distinction, fundraising ability — and, dammit, necessary investing acumen — will lead to massive amounts of consolidation and, of course, outright failure. On the consolidation side, funds who shortfall their raises will begin pairing up with each other. Failures will take the shape of zombie-funds, left behind by fund managers who become disinterested and move on to other projects. And, yeah, there will surely be lawsuits galore. So, for all those new crypto hedge funds out there— how about we just nip this in the bud? Before it grows out of hand? Too prune?