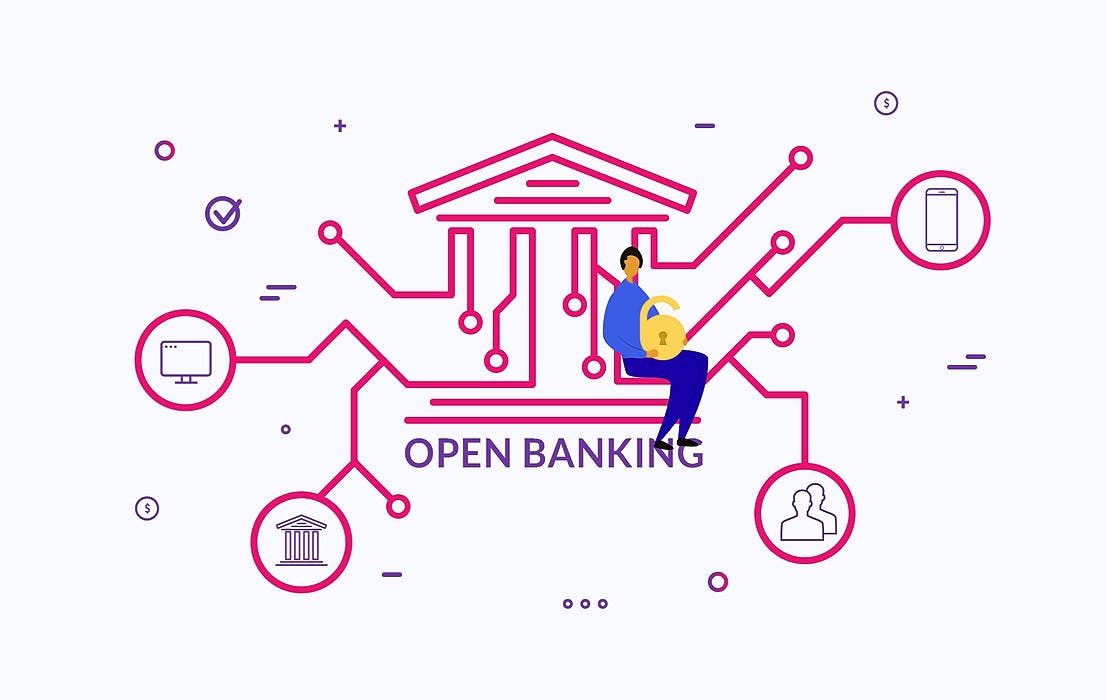

In 2021, India recorded 48.6 billion real-time transactions, more than any other in the world. 2022 Prime Time for Real-Time Crypto, Decentralized Finance, and Smart Contracts might be stealing the limelight from an enormous change in the world of finance that is materializing here and now. That change is Open Banking. The COVID-19 pandemic accelerated the shift from physical to digital mediums of conducting financial transactions. With more time spent online, adopting these new habits accelerated the onboarding of consumers and enterprises – small, medium, and large – to be more accepting of non-traditional financial products and services. Open Banking Definition defines Open Banking as “a banking practice that provides third-party financial service providers open access to consumer banking, transaction, and other financial data from banks and non-bank financial institutions through the use of application programming interfaces (APIs).” Investopedia Open Banking is a global movement in which banks are allowing access to much of the data they hold on to – customer purchases ranging from buying a coffee, a house, or paying mortgages. In open banking, banks typically allow access to their customers' personal and financial data to third-party entities. Examples include , , in India, and many more. Google Pay WhatsApp Payments PhonePe How It Works View the graphic to get an understanding of how Open Banking works. After receiving consent from the customer, access to the customer’s account(s) and data merge with 3rd party service providers like FinTech companies. Opening core banking data to 3rd parties using APIs delivers greater transparency and levels the competitive playing field. Open banking is a driving force of innovation in the banking industry. With the rise in competition on established banks’ turf from smaller and newer banks, it should ideally result in lower costs, better technology, and better customer service. As a result, Open Banking is changing the idea of banking, increasing pressure on incumbents. Value Proposition Open Banking is a driving force of new-age technology deployments that radically transform how finances are handled. The APIs that banking institutions release can look at consumers' transaction data to identify and present the most relevant and appropriate financial products and services. Be it opening a new saving account that can fetch a higher interest rate than the present one or a different credit card with a lower interest rate. Let’s look at the value offerings that Open Banking applications can provide. First, take cues from the UI of the Indian app PhonePe. #1 - Centralised Financial Data Users of Open Banking applications can view their entire payment history in one centralized location. They can even set up automatic payment rules and reminders for due dates. #2 - Intuitive Budgeting Open Banking applications allow users to view dashboards and the flow of funds in different categories. This aids users in understanding their spending habits and sticking to their established budget goals. #3 - Smart Expenditures An Open Banking application user can quickly transfer funds from one bank account to another, receive requests for payments and funds from merchants, and split bill payments without any hassles. #4 - Incentivise Savings Users can receive prompts to increase savings by earmarking extra funds in investment options. Moreover, users can even receive lucrative deals and cashback offers as they continue using their choice of app. Benefits and Drawbacks Consumers and businesses ideally want more choice, ease, and flexibility in managing their money. Open Banking is leading the way to fulfill those wants. Open Banking can help small businesses save time by helping with online accounting and avoiding fraud. Indian payments giant Paytm came up with to make digital payments quick, simple, and safe. Paytm Soundbox However, Open Banking also potentially risks financial privacy and security of consumers' finances, resulting in heavy liabilities to financial institutions. Opening up customers’ data via APIs brings territorial security risks, such as the potential for a malicious third-party app to clean out a customer's account. We’re at the cusp of sweeping and monumental financial industry changes. There are no outright winners and losers yet. Google’s release of maps APIs data paved the way for ride-sharing and other location-based apps to build new products. Similarly, Open Banking has the potential to usher in a new set of innovative products and services that we’re yet to consider viable. Unified Payments Interface (UPI) Introduction Unified Payments Interface (UPI) in India is built on the Immediate Payment Service or IMPS architecture. IMPS was introduced in 2010 and has provided 24x7 instant domestic funds transfer facility. The IMPS system offers a real-time funds transfer between the remitter and the beneficiary with a deferred net settlement between banks. UPI is a centralized facility that does not rely on individual banks. Instead, the National Payments Corporation of India (NPCI) provides the entire facility, an umbrella organization for operating retail payments and settlement systems in India. How It Works The UPI payment mechanism works on the equal participation of 4 intermediaries. #1 - Remitter Bank The remitter bank is the bank of the person initiating the money-sending transaction. #2 - Remitter Payment Service Provider The remitter payment service provider is the UPI app that the person who initiates the transaction uses. #3 - Beneficiary Bank The beneficiary bank is the bank of the person receiving the money from the remitter. #4 - Beneficiary Payment Service Provider The beneficiary payment service provider is the recipient’s UPI app. A Global Case Study UPI is not product innovation. UPI is a distribution, time, and cost innovation. The 2022 Prime Time for Real-Time report reveals that India is far ahead of its global peers. “India led the way for real-time payment transaction volumes in 2021 with 48.6B transactions. The widespread adoption of real-time payments resulted in an estimated cost savings of $12.6 billion for Indian businesses and consumers in 2021. Net savings predominantly drive this in the payment system costs. These savings helped unlock $16.4 billion of economic output, which represents 0.56% of the country’s GDP, equivalent to the output of approximately 2.5 million workers.” Amazing, isn’t it? In the financial year (FY) 2021-22, the Unified Payments Interface processed payments worth $1.09 trillion. In March 2022, UPI achieved another significant milestone. It processed 5.04 billion transactions for the first time, the National Payments Corporation of India (NPCI). according to Even Google has a UPI-like platform to the US Federal Reserve for facilitating digital payments! recommended Upsetting the Established Order The credit and debit cards market has long been a duopoly between Visa and Mastercard. Visa and MasterCard a significant chunk – over 70 percent – of India’s credit cards. With a massive network of customers and merchants across the globe, how does an entity begin contemplating destroying the moat? together process UPI is fast becoming an existential threat to Visa and Mastercard in India. Google Pay, PhonePe, and Paytm have managed to coax consumers to replace cash for many use-cases. As a result, they might soon be on the turf of the credit card industry. With Russia no longer a part of the SWIFT system used for cross-border international payments, explored alternate payment systems to ensure bilateral trade continued. One option included linking the Indian Unified Payments Interface (UPI) with the Russian Faster Payments System (FPS). Russia and India Closing Thoughts In this piece, we learned from the ground up what is Open Banking, how it works, and why we should seriously consider its value proposition. Furthermore, we learned how India with its Unified Payments Interface (UPI), is a global case study to learn from. Open Banking, if implemented properly, can revolutionize the world of finance and even break the hegemony of established institutions – potentially ushering in revolutionary product developments.