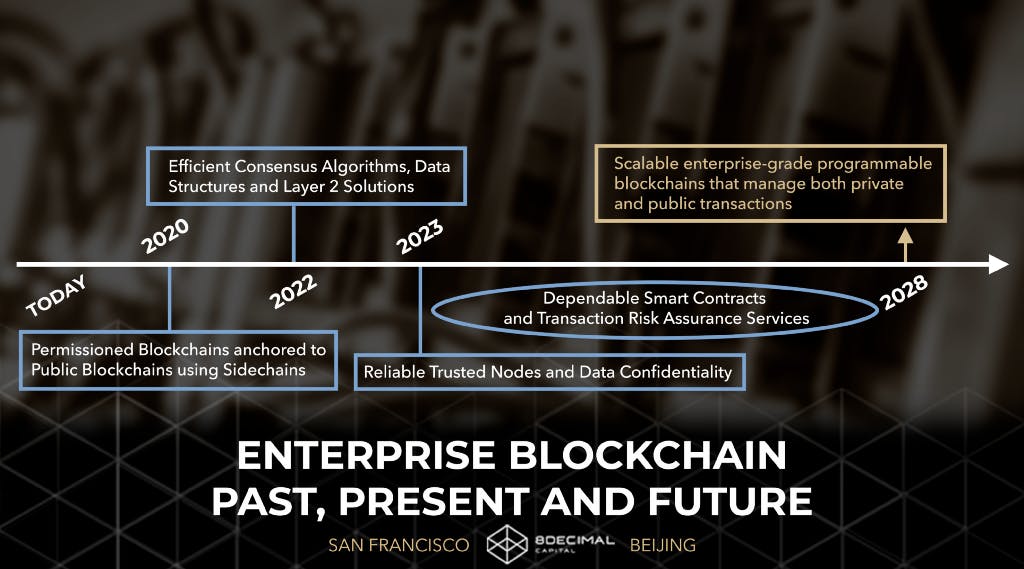

I had the pleasure of presenting on the topic of “ ” in January 2019 at the conference in London. Below is a summary of some key ideas from the presentation. If you are interested in learning more about our insights and perspectives on investing in the space, check out the . Investing in the Security Token Ecosystem Security Token Realized full video presentation here I) Key Benefits of Security Tokens: : Establishing trust between different parties is of vital importance locally, nationally, and globally. Blockchain is the ultimate cap table of “who owns what” and a record of all the previous transactions. Additionally with smart contracts, we can program compliance so that trades can automatically go through if the investors are compliant, else there would be an error blocking the transactions. This can make transactions a lot faster and cost-efficient. Transparency & Programmability Right now buyers and sellers can’t find each other, and need to go through their fund managers to make their transactions happen because of all the contractual rules enforcing “who is trading / what assets / where are the trades taking place”. This can take months or years to get out of established positions, creating a lot of risks for the investors. Liquidity: Blockchain allows for digital assets to be portable for different platforms and exchanges because they are sharing the same technology layer. This is something that wasn’t possible since currently, each technology company is a closed system. By utilizing a common layer that we can all trust, we can allow for a truly global market. 24/7 Market & Portability: Before emails came out, people were using Snail-Mail to send a message, in which you had to print out the message, put it in an envelope, pay $0.50 and wait 3 days for the mail to be delivered. Later came emails, and with one click, you could send over your message instantaneously, with an order of magnitude faster, cheaper and with much more simplicity. In a similar way, with tokenization you can allow securities to have an electronic format, drastically lowering the cost, easily tradable and interoperable on different exchanges. Cost Reduction: The fact that issuing tokens is much cheaper, and simpler than the traditional way, we can essentially enable use-cases and business models that weren’t practical before. For example, prior to email, you wouldn’t mail a letter to someone to schedule for lunch, but now you can do it through email. And this is something that we think a lot about, especially with the potential for new industries and business models to emerge from new technology. This doesn’t exist in the market yet, but for example, tokenizing a sports team, let’s say the Celtics. Right now you could sell the ownership of the team to a major investor, but if the cost is low enough, you can tokenize 10% of the team and sell it to 2000 people, which is the maximum holders you can have for a single class of equity, the token can allow for dividends, capital appreciation, and have other interesting features, such as first dibs on box seats, meet players after the games etc. If you were to do it right now, it would be a pretty complicated and expensive process of managing everybody’s assets. This fits well with some of the consumer trends we see with Netflix and Spotify, in which consumers prefer having experiences over ownership of products. With security tokens, you could allow for fans or mainstream investors to have ownership into their favorite team and potential access to new experiences. Conclusion: Overall, 8 Decimal Capital is looking for an evolution rather than a revolution: we are expecting a hybrid digital world instead of a purely digital world, because we would still need central authorities to provide us the ultimate protection. This hybrid world combines the traditional business world with new technology, without completely replacing current business structures. We think tokenized securities will not replace all financial services. Tokenized securities will simply provide better tools. For example, Salesforce didn’t replace salespeople, but simply provided better tools for salesmen. In the same way, tokenized securities can help companies, brokers, and investment banks raise money more efficiently, but they will still exist. So security tokens will not remove all the middlemen, but make the processes work more efficiently. II) Hype Cycle of the Security Token Space: This is inspired by the hype cycle charts that Gartner usually creates for emergent technologies. Early Stage As of now, we are still in the early stages of the Security Token ecosystem, in which different issuance solutions and exchanges are still being developed and tested. We believe that it will take about 4 years for the STO ecosystem to grow and mature from both a technical and regulatory perspective, allowing for a sustainable transition of the traditional system. Until the space becomes more mature, the majority of the early adopters of STs are going to be from the cryptocurrency space rather than from traditional institutions. As the different STOs and exchanges launch this year, we predict that the lack of liquidity, as seen through the low liquidity on some of the security exchanges and challenges around implementing complex use-cases and securities laws, will bring us closer to this digital reality and decrease the overall hype and expectations around STOs. Security Token Illiquidity: We have spoken to dozens of projects launching exchanges for security tokens, and we always ask them the same question “How will you create liquidity for the tokens listed on your platform?” Oftentimes, they answer this question by mentioning the market making institutions they will partner with. In our opinion, this method won’t produce the results needed in the space. Market making institutions can create liquidity for those exiting a position, but they won’t be able to sell the tokens for a profit if there isn’t a real and substantial demand on the buyers’ side. Prior to liquidity, the players in the space might be better off focusing on the more traditional model of broker-dealers, capturing fees by connecting great projects with investors, and minimize the need for tokenization until the industry becomes more mature. The path to Adoption: In the future, major traditional exchanges, such as the Nasdaq, will also develop their own solutions to facilitate the trade of security tokens in 2019. We have seen a recent project, Bakkt, created by The Intercontinental Exchange (ICE), an operator of several global exchanges including the New York Stock Exchange, just raise over $182M in funding to enable consumers and institutions to buy, sell, store and spend digital assets. It would be very easy for them to offer security tokens down the line. How would we know that the industry has reached a mature stage? Overall, on the technology side, blockchain technology still has a lot of friction in terms of usability and we need a lot more user-friendly UI/UX. We know the industry is mature enough for adoption when using blockchain-based technology will feel like using regular, mainstream softwares, so that we can focus more on the quality of investment projects rather than focusing on dealing with the short-term limitations of the technology. Over time, more efficient technology and new regulations will appear and help drive the growth and adoption from the traditional players. III) Our Investment Criteria in Security Token related Projects: These are several high-level criteria that we have for our investments in the space. However, our decision also depends on factors that are not discussed in this article and we will consider alternative edges that are outside of this framework. Since most of the projects are in their early stages, we focus heavily on the team’s background. We prefer teams who have worked in the financial or crypto industry, with previous start-up & exit experiences. In the case of a security token exchange, ideally, the founders have the combination of both. Overall, the existing cryptocurrency exchanges are more familiar with crypto trading, but they often do not have the necessary licenses in place, while the traditional exchanges are the opposite. Team: We have seen a lot of projects getting licenses from small places that have security token-friendly legislation. Due to the size of their governments, these countries are able to adapt at a quicker pace than larger countries. However, we prefer if the licenses are from larger countries, such as the US, Singapore, and European countries instead of small places like Gibraltar, Mauritius, and Malta. Large countries would give more credibility to the company down the line and unlike ICOs, many regulators around the world are showing positive sentiment towards the STO market, even the SEC, so it’s just a matter of time before specific regulations for digital assets become more official. Licenses: In addition, it is important to know where the projects received their licenses, whether its an ATS (Alternative Trading System License), RIA (Registered Investment Advisor Licence), BD (Broker-Dealer Licence), or RAE (Clearing and Transaction Execution Licence). We also pay attention to whether they own their licenses or are utilizing a third party’s license, oftentimes for a revenue split. If it’s from a third party, then we would like to get more details on the terms of the partnership. All things considered, we are trying to select the companies that have the best shot at succeeding in this new emerging market. Similar to the approach taken by Don Valentine from Sequoia, we really focus on understanding the emerging market, how it could potentially evolve, and pay attention to the different players in the space. Our job is essentially to identify the companies who can be a good fit to execute in this market. Competitive Advantage: We have seen a lot of security token exchanges and issuance platforms which have too big of a valuation. We think this might be due to the previously inflated valuations and frenzy from the cryptocurrency bull run. If it is just a team with an idea without any licenses or technology, the valuation should be under $10 Million. If they do have an edge around licenses or technology, then the valuation can go up to $20 Million, and depending on traction, up $40 Million. Valuation: It’s probably not the most important component because we’re early and you can fairly quickly switch and catch up on technology once a better solution is proven to be more successful. But it helps to understand how the entrepreneur thinks about tokenization and how much thought is put into considering the compliance requirements (investor whitelist, trading permissions in smart contract, backdoor to help on re-issuing security tokens if a major problem occurs etc.), regulatory limitations (GDPR around data), disclosure, privacy etc. Technology: It is important to understand that unlike cryptocurrencies, security tokens do not represent ownership, but a record of ownership. This is fundamentally different and necessary because if an investor loses his/her private keys or is deceased, you should be able to cancel token ownerships and issue new ones. Shares of a company cannot disappear out of thin air if the company is still there. And this is also why we think the future will be a hybrid model instead of a fully digital one. This type of back-door mechanism is available in Harbor, for example. We have our own opinion but we always keep an open mind to hear how the entrepreneurs are planning to tackle this industry, how they think about the space, and the timing of releasing products in order to build a sustainable business. For example, if the maturity of the industry is not there and cannot provide liquidity, then focusing on finding great projects, tokenizing them and bridging capital from traditional investors might make more sense at this stage, then launch the exchange business once the industry matures and has more liquidity. Basically, build the company according to the growth and maturity of the industry. Go-to-Market: IV) What Type of Assets are Good Candidates to be Tokenized First? As we are early in the industry, it’s important to identify which assets make more sense to be tokenized first as different assets will have their own requirements and frictions. We recently sent out a questionnaire to 20 of our partner channels, asking what they would prefer investing in, within the frame of tokenized products. The majority of respondents preferred real estate and fixed income producing assets. The last thing they want is actual equity. People are currently looking for more stable assets, even with small returns of 3–5%. They prefer something in which the model is clear, for example, if you buy airplanes and rent them, you can easily forecast revenues vs investing into the equity of a startup. What makes sense to tokenize at this point in time, is also things that are capital intensive and when the identity of the investor does not matter too much, as long as they are legal. For example, real estate is a good example in which you can unbundle into smaller units of investment, gather funds from investors around the world, and lower the cost of capital vs investing in tech startups. Additionally, early-stage tech startups wouldn’t like investors trading around their equities, in which speculations can inflate or kill their valuations, and affect their growth. Security tokens aren’t the new ICO. It’s better suited for companies with more stable revenues in which the value of the tokens can be correctly assessed. We think another good way to think about which asset class to tokenize first would be based on how much information you need to know on the investor side to make this happen. The less information you need, the less friction there would be on the adoption. Currency is easiest to tokenize as you don’t really need to know the information about the investors (nobody tracks who owns cash), followed by commodity, then real estate, and finally equity, the most complex asset, which requires the most KYC/AML. This is the approach taken by TrustToken, which is first focused on Stable Coins. As of right now, you don’t need to know the identity of everybody holding TUSD, just like you don’t need to know who’s holding cash, but this might change in the future. And finally, this is often overlooked by platforms right now. We think a lot of the security tokens coming out this year won’t be of high quality, as many are chasing the hype and utilizing this opportunity to raise capital. However, at the end of the day, for a project to be liquid, it still has to be fundamentally strong, offering real value, else even in a tokenized form, it will remain an illiquid asset that no investors would want to purchase or trade. Please let me know your comments, and feel free to reach me out at remi@8dcapital.com if you have any more questions about this topic.