8,318 reads

Crypto: Traders’ Paradise, Investors’ Hell

Too Long; Didn't Read

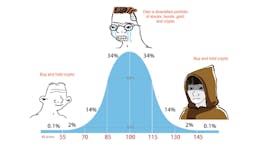

Cryptocurrencies have been massively rewarding for both early investors and savvy traders. Take bitcoin for example. All those who invested before 2017 have seen returns greater than 550%. Traders on the other hand greatly benefit from bitcoin’s significant volatility: one day of bitcoin volatility is nearly equivalent to volatility of an interval of roughly <a href="https://medium.com/@cryptoquantamental/the-dog-days-of-crypto-a9d33670ffbe" target="_blank">23 trading days for the S&P 500</a>. For traders, volatility brings opportunity.People Mentioned

Companies Mentioned

Coins Mentioned

Alex Krüger

@alexkruger

L O A D I N G

. . . comments & more!

. . . comments & more!