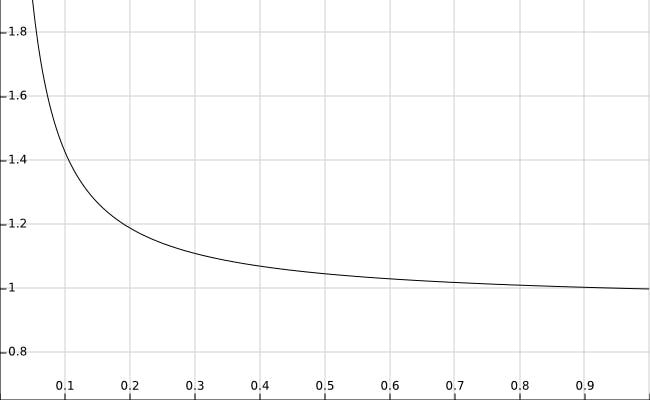

How stake deposits affect mining profitabilty Costs and risks of stake deposits In a Proof of Stake blockchain, stakeholders are typically required to make a stake deposit in order to become miners, also called validators (systems that merely require momentary coin ownership for creating blocks are prone to nothing at stake attacks and aren’t considered here). They have to lock up funds for a certain amount of time determined by the protocol. Security deposits thus involve a number of costs and risks that must be borne by the validator: The validator cannot use or invest his stake otherwise during the lock period. Capital lockup (liquidity) costs: If the cryptocurrency is inflationary, the deposits are subject to dilution as new coins are emitted by the system. Dilution: The deposits might depreciate while they are locked. Exchange rate drop: : The validators must have appropriate hardware to run a network node and will need to pay for the electricity and the internet connection, even without having to perform heavy computations like in Proof of Work. Computational work, storage and bandwidth System failures and DDoS attacks against the validator’s node may result in penalties or in worst case in a total loss of the deposit. Loss of the deposit or penalties imposed by the system: Coin emission and its effect on mining profitability To incentivize mining, the rewards for creating blocks have to compensate for all the costs and risks incurred by the miners and provide an expected net gain in the end. The higher the profits, the more stake will be used for mining in general (marginal costs = marginal revenue), stirring the competition between validators. This is desirable as it makes 51% attacks more costly. For maximal security, it is therefore crucial to maximize the overall profitability of mining. In existing blockchains, rewards are either funded by transaction fees or newly minted coins. Let’s focus on the latter for now. By the emission of new coins, the value of the currency is constantly diluted as the market capitalization gets spread across more and more currency units. In the following, we will analyze how that affects the miners’ stake deposits. Stakes deposits in native cryptocurrency Imagine a blockchain that applies a yearly coin emission rate of 5%, i.e. pays out 5% of the total currency supply as newly minted coins to the validators in proportion to their deposits made in the cryptocurrency native to the system. Let’s assume, furthermore, that the market capitalization of the currency remains constant for a whole year. As the value of a currency unit is given by the market capitalization (expressed in USD or another fiat currency) divided by the number of coins in circulation, every owner who kept all his coins without being a validator will end up with 95.24% (= 1/1.05*100) of his original investment by the end of the year. Note that the 4.76% loss of value is a result of the inflation and does not depend on the number of active validators or the total amount of stake used for mining. On the other hand, the real value of the validator’s deposits will heavily depend on these factors. For example, if 10% of the stake participates in mining, a validator will receive 50% (= 0.05/0.1) nominal interests on his stake deposit. However, if we look at the real value of his investment at the end of the year, the increase is only 42.29% (= 1.5/1.05*100) since miners are affected by inflation just like any other stakeholder. If is the fraction of stake that is actively mining and the coin emission rate, the real value of a validator’s total balance after one year (assuming a stable market cap) can be expressed by b(f, p)= (1+p/f)/(1+p). f p For p=0.05, the plot of the balance function b(f, 0.05) looks like this (with f on the x axis): We clearly see that as the fraction of actively mining stake approaches 100%, the balance goes down to 1, i.e. the real return on investment drops to 0. The reason is that with a stable market cap, all rewards must come from the dwindling fraction of stake that is not involved in mining. To calculate the total fraction of stake that can be deposited to achieve a certain real return, all we need to do is solve the equation b(f, p) for f, hence f = p/(b*p+b-1). If validators are willing to deposit stake as long as their real return is at least 4% (b = 1.04), f will equal 0.543, that is 54,3% of the stake would be used for mining in our example. As a result, the market capitalization of the currency will put an upper limit to how much value the system can effectively pay out to its validators. This limit exists regardless of the nominal coin emission scheme and means that potential miners with high expectations will be deterred by the small profit margin. Other than that, the maximum deposited amount is capped by the total currency supply. Obviously, there cannot be more stake deposits in aggregate than amount of stake available! Therefore, an adversary with funds worth half the currency’s market cap can acquire majority power over consensus in any case. In practice he will need much less capital though since only a fraction of all coins will be used for mining at all times. Hence, a Proof of Stake system’s financial security against 51% attackers in the individual choice model (i.e. we rule out collusion and bribing) will basically be a function of its market value and the fraction of actively mining stake. Can we do better than that? Stake deposits in foreign cryptocurrency What if we require the validators to make their stake deposits in other cryptocurrencies than the system’s native currency? If the foreign cryptocurrency is based on a platform that allows meaningful smart contracts, one can create a contract that locks the deposited amounts and releases them on receiving an unlock transaction signed by the native system. The latter would issue an unlock transaction after the minimum lock period, provided that the miner acted by the rules of the native cryptocurrency. By using forex for deposits, we can firstly lift the theoretical limit on the deposited amounts. The total deposits can now exceed the market capitalization of the native currency. But what about the depreciation of the stake deposit caused by an inflationary coin emission scheme? The real value of the validator’s end balance after one year is now given by the formula b(f, p)= 1+p/f, where f is the fraction between the market value of the total deposits (in foreign cryptocurrency) and the capitalization of the native cryptocurrency. The balance function still depends on the fraction of actively mining stake and asymptotically approximates 1. But in contrast to stake deposits in native cryptocurrency, there will be a positive yield even if the total bonded stake exceeds the market capitalization of the currency. We can again solve the balance equation for f = p/(b-1), and calculate it for b=1.04 (minimum end balance) and p=0.05 (coin emission rate), so that we get f=1.25. In other words, 125% of the stake will be used for mining, which is more than double of what we had in the previous example (54.3%) where the native cryptocurrency was used as a security deposit. . As we can see, when the stake deposits are made in a foreign cryptocurrency, it is possible to have security deposits worth more than the native cryptocurrency’s market cap In such a case, the costs to get majority control aren’t capped by 51% of the cryptocurrency’s total value. Advantages of forex stake deposits To illustrate the security advantage of forex stake deposits over deposits made in native cryptocurrency, we can calculate the f_foreign(p, b)/f_native(p, b) = (b*p+b-1)/(b-1) and plot the function for both variables p and b separately. For b = 1.04 and p on the x axis, we get the following curve: We see that the advantage of forex stake deposits over deposits in native currency grows with an increasing coin emission rate (since the dilution of native currency deposits gets higher). On the other hand, we can fix p at 0.05 and plot the function for the expected balance at the end of the staking period on the x axis: The diagram tells us that the advantage of forex stake deposits gets higher as the expected real return gets lower. So, are forex stake deposits always preferable over native currency deposits? No. If the foreign cryptocurrency itself is inflationary, the stake deposits will be subject to dilution depending on the emission scheme of the foreign cryptocurrency given that they aren’t used for minting the forex cryptocurrency. In that case, the stakeholders must factor that into their return expectations. Luckily, this problem can be mitigated by staking non-inflationary cryptocurrencies or stablecoins that are pegged to a fiat currency. Also, if the deposited cryptocurrency is mined by Proof of Work, there’s no inherent possibility to account for the inflation other than by performing computational work. So, a stakeholder of that currency who is not able to mine (profitably) anyway will be better off by becoming a validator of the native cryptocurrency. Using a foreign cryptocurrency for stake deposits has two other notable consequences that we leave undecided: Some argue that in Proof of Stake, the real value of the deposit is also at stake, which prevents validators from doing harm to the network as it would depreciate their staked funds. This should, for example, offer protection against an attacker who is trying to bribe the stakeholders into malicious activity. With stake deposits in foreign cryptocurrency, this protection no longer applies. However, even if native currency is used for staking, it remains unclear if the actions of a minority stakeholder can be pivotal with regard to the exchange rate. If a majority or a higher number of stakeholders must concur to negatively impact the price, every individual actor could still have a personal incentive to contribute (i.e. accept a bribe), regardless of the consequences that the group’s behavior could have as a whole, resulting in a tragedy of the commons. On the other side, if an attempted attack or its announcement exerts a downward pressure on the price of the native cryptocurrency, it becomes cheaper for the attacker to buy the amount of stake required for majority control. This is not the case with stake deposits in foreign cryptocurrency whose value remains unaffected by the attack. One caveat is though, that the rewards are still paid in the attacked system’s native cryptocurrency, so their real value will in fact be affected. On the short run, this shouldn’t have a big impact since stakeholders cannot withdraw their deposits all at the same time due to the lock period. If the threat persists for a longer time, the total deposited amount will gradually decrease and approximate MR=MC again. Conclusion By staking foreign cryptocurrency, we can eliminate the due to an inflationary emission scheme of the native currency, provided that the staked currency itself is not inflationary. We can also mitigate the if a stablecoin is used for bonding. dilution costs exchange rate risk You may ask if we can do even better and remove the c_apital lockup (liquidity) costs_ as well. This will be discussed in Part 2 of this series. Stay tuned!