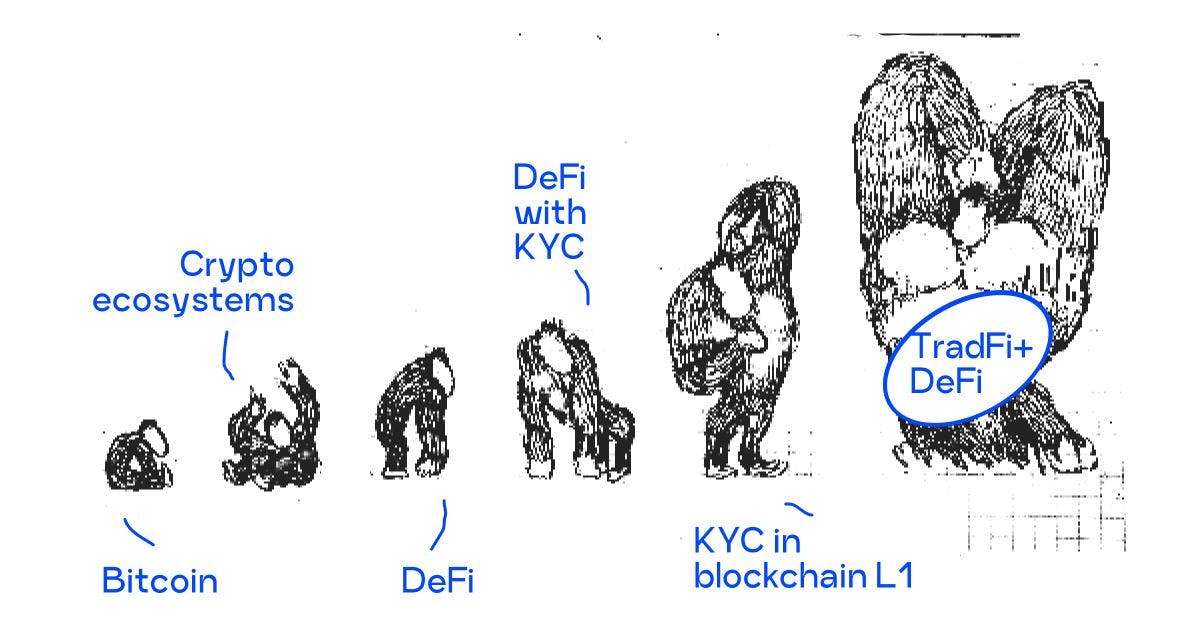

With every new day, I begin to believe that history goes in circles. The crypto industry nowadays reminds me of the Wild West. It’s gold rush time, and instead of making profits from gold itself, some people build great infrastructure that will last for dozens of years, while others look for opportunities to make a fast but unsustainable profit. If we compare what’s happening in the DeFi industry now to what was happening back in the 19th century during the formation of the traditional banking system we’ll see a lot of similarities. TradFi has long gone through a similar stage in the evolution of its system, and it is not ready to plunge back into the same chaotic state again. People of TradFi love to have streamlined processes, guidelines for everything, different norms, and rankings based on what is important for the system they’ve built and maintained for a hundred years. But the current state of DeFi, with its constant changes, new projects being created every day, and the ever-present paradigm of “breaking the paradigm” denies the possibility of instant integration into a more polished and unified ecosystem of traditional finances. And don’t get me wrong, I don’t see TradFi regulations as a problem. To put it simply, I see it as a set of instructions on how to interact with the traditional system. TradFi has to stay clean to work, so they came up with KYC procedures. And it became one of the greatest issues standing in the way of integration between DeFi and TradFi. The Great Wall TradFi is looking for the cleanest and most streamlined ecosystem they can get (even though sometimes bureaucracy drives me crazy), and DeFi as a pile of unique protocols doesn’t work this way. Take a look at the number of stolen funds through DeFi hacks tripled in 2021, according to Ciphertrace’s . This alone would be enough of an argument for traditionals to scrap the idea of merging the traditional and decentralized finances into one seamless ecosystem. “Cryptocurrency Crime and Anti-Money Laundering Report, August 2021” I know a couple of L2 projects that have already tried implementing the KYC procedure despite all odds. Apart from that, it’s safe to say many of them succeeded, but they didn’t plan far enough. L2 KYCs exist and work, providing the founders with the title of mediator between TradFi and DeFi. Or at least that’s what they thought before people got the thought that KYC should also be flexible to fall within the regional regulations and other preferences while also have a certain standardization level to become a single industry-wide solution. It’s a matter of perfect balance between flexibility and unification pioneers will have to achieve. Such a solution will not only reduce the number of hacks but will also establish the basis for the further growth of both traditional and decentralized ecosystems. Unfortunately, the and such giants as PayPal, Robinhood, E*Trade, and Stripe didn’t lead to any serious results, but having that dialogue in the first place is already a giant step forward, and I’m sure we’ll soon witness a flood of news regarding the KYC/AML topics in DeFi. public dialogue between Uniswap L2 is missing a couple of important points I’m still assured that KYC built on L2 is a temporary solution. Such projects became an island of safety in the DeFi industry, and it might sound good but not good enough to shape the financial industry as a whole. Another problem that comes to mind is L1 anonymity. If an L2 KYC solution is built around an anonymous L1 blockchain, then interacting with other projects built on the same blockchain wouldn’t be possible. What’s the point of having a KYC if you have to complete it again and again for every product you use? First — it’s inconvenient when it comes to UX/UI. Second — projects allocate additional computing resources to process and safely store private user data. And to sweeten the pill, every product uses its KYC standard depending on the region of operations. Based on the 2017 research by Consult Hyperion financial institutions have been reported to spend $60 million on KYC checks annually. Some are spending up to $500 million on KYCs each year, according to the . This leaves us with a very understandable demand for optimizing the maintenance costs of current KYC solutions. 2016 Thomson Reuters survey At the same time, some of these projects never passed any audits except for the internal ones. Lack of safety concerns already led to data leakages and also contributed to the shady reputation of the decentralized ecosystems. KYC should be L1 Let’s be honest here, while blockchain is good at handling a lot of things, centralized storage algorithms are more convenient for the storage of sensitive user data. First and last name, address, photo, or even passport info might be doxxed after a single smart-contract breach if you keep KYC applications on-chain. As I see it, authorized KYC centers around the world do a better job of storing and verifying user data while also bringing the collateral damage from a breach to a minimum. The KYC verification procedure can take place off-chain, with a randomly chosen KYC center, and the verification results will be sent back to the blockchain. This will also allow for better interactions within the network itself, and users of such a blockchain would need to pass the KYC procedure only once. After that, the user will be free to use the same account to interact with any other product launched on said network. We’ll also need to come up with a reward mechanism for KYC centers if we want to keep the network clean of fake confirmed accounts because even the possibility of such shady operations would also paint the whole network in all shades of gray and black. And as we already know, TradFi doesn’t really like that. The KYC procedure itself should not be forced upon users and must consist of several levels or tiers. For example, a basic one with email verification, a middle-ground level with documents, and the maximum tier with a video confirmation. This way the solution doesn’t exclude those who wish to stay anonymous, while other users or entities can set up a filter for a certain level of KYC verification that your counterparty must have. I’ve been working on building a draft of an L1 KYC-oriented blockchain for a couple of months already. Even in TradFi, there are just too many unsolved challenges in the field of international KYC/AML procedures, not to speak of blockchain. But blockchain is famous for being a cross-border technology, and if we take into account all possible requirements the TradFi has, it doesn’t seem like that much of an impossible development. TradFi took a hundred years to establish, and take a look at what DeFi achieved in just ten. The process has already begun! Thanks to everyone who made it to the end, I would appreciate questions, and the only thing I’d enjoy more than receiving questions would be answering them. First Seen At https://medium.com/@bobstewell/blocks-docs-and-two-blockchain-layers-the-future-of-kyc-on-l1-88eed9a02607